WBCSD’s TNFD pilot

Purpose

This resource provides a synthesis of the WBCSD Taskforce on Nature-related Financial Disclosures (“TNFD”) pilot process, summarizing pilot member business experience, learnings, challenges, illustrative applications and examples. Reflections draw on multiple sources including group workshops, spotlight sessions, bilateral discussions and TNFD maturity assessments. It is intended to provide insights for companies working with the TNFD Framework and practical ‘how-to’ guidance on the TNFD’s LEAP approach (including three use cases) and disclosure recommendations. The pilot was conducted with 23 WBCSD member companies, in collaboration with PwC UK*, as part of broader work on Nature Action and Redefining Value in WBCSD.

*In this resource, "PwC" refers to the UK member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

Note

The TNFD pilot started in September 2022 based upon beta v0.2 of TNFD guidance and continued through beta v0.3 and v0.4 until June 2023. Accordingly, the piloting content was regularly updated according to the latest TNFD framework release.

While the pilot was conducted with beta versions 0.2, 0.3 and 0.4 of the TNFD framework, this resource includes version 1.0 of the TNFD recommendations where relevant, unless expressly stated otherwise.

WBCSD requested PwC’s support to set up and run the pilot, including the use of PwC UK’s TNFD maturity assessment methodology. The methodology is designed to provide organizations with an understanding of their maturity in relation to the TNFD and wider nature landscape. WBCSD and PwC have collaborated in designing and executing this pilot throughout, and this resource is published by WBCSD with support from colleagues at PwC.

In addition, WBCSD engaged Environmental Resources Management (ERM) to provide additional support, in particular for the energy pilot.

Throughout references are made to various third party third-party nature-related tools and data providers. These references do not reflect endorsements by WBCSD or PwC UK but rather are stated as examples that were identified during this pilot process.

This content has been developed in the name of WBCSD. Like other WBCSD publications, it is the result of collaborative efforts by representatives from member companies and external experts. A range of member companies reviewed drafts, thereby ensuring that the material broadly represents the perspective of WBCSD membership. Input and feedback from stakeholders listed above was incorporated in a balanced way. This does not mean, however, that every member company or stakeholder agrees with every word.

The resource has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and to the extent permitted by law, the authors and distributors do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Introduction

- Why was this pilot conducted?

- How was the TNFD pilot conducted?

- Introducing the TNFD framework

- Pilot members’ TNFD maturity

Nature loss poses both risks and opportunities for business, with over half (55%) of the world’s gross domestic product (GDP) moderately or highly dependent on nature, equivalent to an estimated US $58 trillion . However, many businesses don’t have a comprehensive understanding of how their activities, positively or negatively, impact nature or how nature will impact their business’s financial performance both immediately and in the longer-term.

The Taskforce on Nature-related Financial Disclosures (“TNFD”) was launched in 2021 with the ultimate aim of supporting a shift in global financial flows away from nature-negative outcomes and toward nature-positive outcomes. It provides a voluntary risk management and disclosure framework for businesses to report and act on evolving nature-related risks which will allow financial institutions (“FIs”) and companies to incorporate nature-related risks and opportunities into their strategic planning, risk management, investment and financing decisions.

The fact that much of the language of Target 15 from the Global Biodiversity Framework (“GBF”) (signed in Montreal in December 2022), mirrors that of the TNFD, is a testament to how this framework is already being used by policy-makers and businesses to identify, assess and disclose their nature-related dependencies, impacts, risks and opportunities (“DIROs”). Furthermore, the number of companies reporting DIROs under the framework, is one of the official monitoring indicators for the GBF’s Target 15.

In 2022, the World Business Council for Sustainable Development (WBCSD), Business for Nature, Capitals Coalition, TNFD, Science-Based Targets for Nature (SBTN), World Economic Forum (WEF) and World Wildlife Fund (WWF) collaborated to provide business with a consistent approach to accelerate nature action. Leveraging WBCSD’s Building Blocks for Nature Positive alongside other key frameworks, this group developed the high-level business actions on nature , also known as the ACT-D framework: Assess, Commit, Transform and Disclose.

WBCSD has engaged more than 75 member companies to develop detailed Roadmaps to Nature Positive, which provide step-by-step guidance on this journey, including how to get started, and progress on ACT-D across all maturity levels, backed up by deep dives into specific value chain systems. The deep dives into prioritized value chains are supporting companies in scaling up actions to halt and reverse nature loss, prepare to set science-based nature-related goals and targets, and disclose progress using quantifiable metrics.

|

To learn more about this work, see WBCSD’s Roadmaps to Nature Positive – Foundations for all businesses Explore the foundations for specific systems:

Overviews for additional sectors are available on Business for Nature. |

WBCSD was selected as a piloting program partner to test and inform the design and development of the TNFD framework through knowledge sharing and provision of feedback. Input has been provided on an ongoing basis to the TNFD secretariat on the TNFD beta versions over the 12 months prior to the release of v1.0 of the TNFD framework in September 2023.

WBCSD member companies welcomed the opportunity to unpack TNFD framework components and share learnings and reflections, whilst leveraging experiences from WBCSD’s Taskforce for Climate-related Financial Disclosures (“TCFD”) Preparer Forums, Nature Action, Redefining Value and strategic value chain Pathways programs, plus experience with the Natural Capital Protocol.

A cohort of 23 WBCSD member companies were selected to participate in the pilot, representing a range of geographies and businesses, with three groups reflecting the socio-economic systems with potential for significant impacts and dependencies on nature:

The Land-based (Agri-food and forest) system impacts 72% of species under threat by contributing to water and soil pollution, deforestation, land degradation and habitat destruction.

The Built Environment (Infrastructure, Real Estate & Construction Materials) system impacts 29% of species threatened with activities driving increased flood risk, water, oil pollution and degradation of land and seabeds.

The Energy and Extractives (Oil & Gas, Electric Utilities, Bioenergy, Metal and Mining) system potentially impact 18% of species threatened, through activities that may contribute to land use change, freshwater use, pollution and landscape alterations.

These systems also present significant in ensuring a transition to a low carbon, nature-positive economy.

The pilot provided a space and structure for companies to learn about and engage with the TNFD framework, and as a consequence, provide user feedback as the framework evolved. Sector-specific learnings, experiences, challenges, case studies and suggestions were all synthesized and shared with the TNFD secretariat for consideration in the iterations of the TNFD guidance.

- For more information on pilot summary feedback to the TNFD, please download appendix I here.

- For more information on commonly asked questions by TNFD pilot members, please download appendix II here.

- For more information on approach and methodology, please download appendix III here.

- For more information on organizations engaged throughout the TNFD pilot, please download appendix IV here.

The TNFD Disclosure recommendations

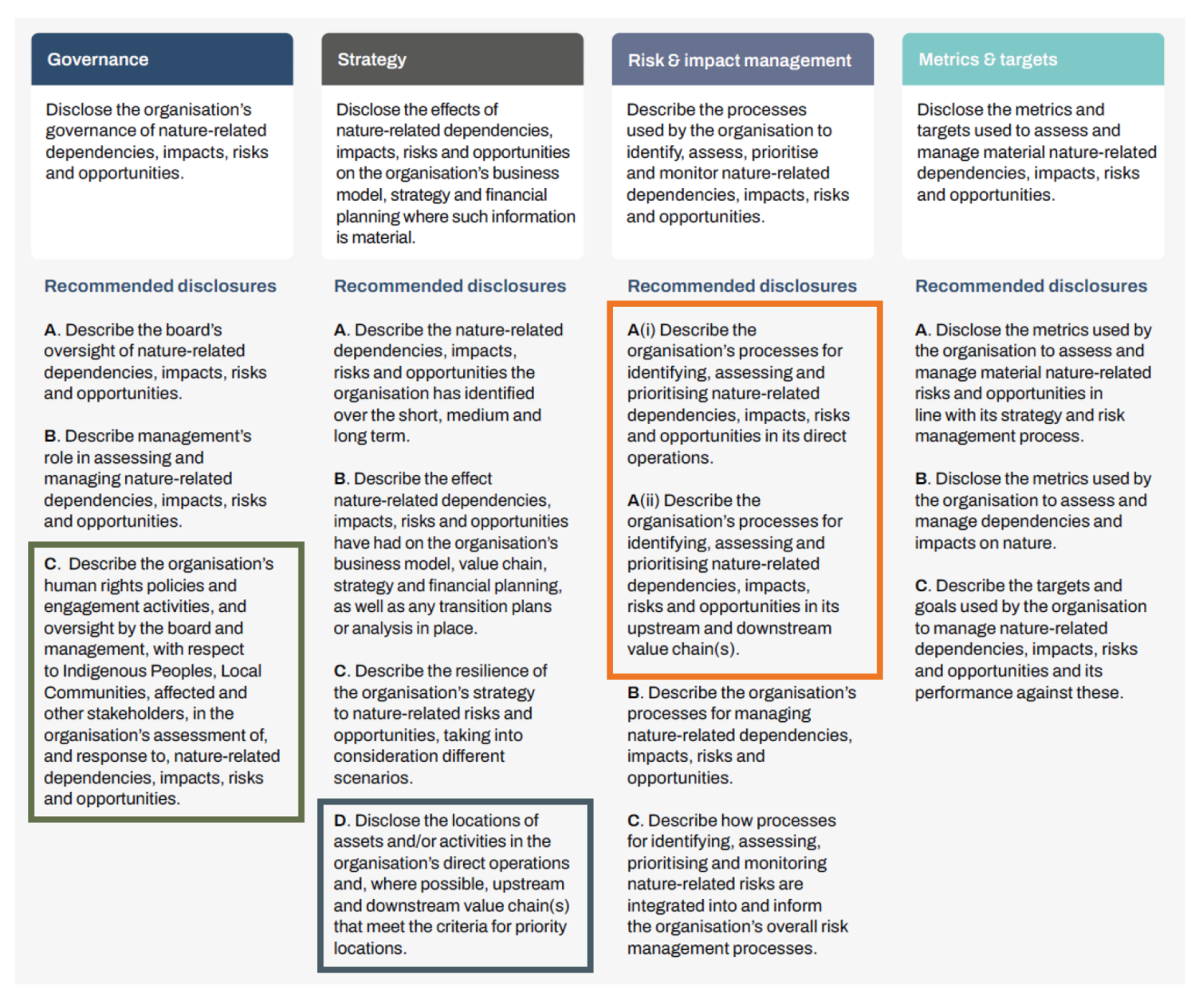

The TNFD has developed a framework for nature-related risk and opportunity management and disclosure with the aspiration to inform, and feed into, the specific standards developed by organizations such as the International Sustainability Standards Board (“ISSB”) and specific market regulators. The TNFD recognizes the interconnectedness between climate and nature-related issues and encourages an integrated approach to risk management and disclosures. The framework outlines disclosure recommendations that are aligned to the TCFD, with organizations encouraged to disclose around four key pillars: Governance, Strategy, Risk & Impact Management, and Metrics & Targets (see here).

Figure 1:TNFD’s recommendations and recommended disclosures

Source: TNFD (2023). Taskforce on Nature-related Financial Disclosures (TNFD) Recommendations. Retrieved here.

Each of the four pillars are split into recommended disclosures. All 11 of the TCFD recommended disclosures are either included or have been slightly adapted. One exception to this is that the concept of Scope 1, 2 and 3 emission reporting in the TCFD has been changed to reflect direct, upstream, downstream and financed activities. This is reflected by the fact that the ‘Risk and Impact Management A’ disclosure recommendation (in the orange box) has been split into two parts:

● A(i), covering direct operations; and

● A(ii) covering upstream, downstream, financed activities and assets. This allows differentiated approaches to nature-related issues in direct operations and value chain(s).

In addition to these 12 disclosure recommendations, the TNFD includes 2 additional disclosure recommendations:

● Strategy D (in the blue box), covering priority locations; and

● Risk and Impact Management D (in the green box), covering stakeholder engagement

However, despite the similarities between the TCFD and TNFD frameworks, one of the challenges of the TNFD when compared with the TCFD is that there is no single metric of measurement for nature change (like the carbon dioxide equivalent, CO2e, for climate). This creates challenges for businesses trying to aggregate nature-related issues up to the company-level for reporting purposes, or for comparison across business units or geographies. The TNFD have worked to take these complexities into account and provide a simplified, systematic process accounting for these differences. On numerous occasions the TNFD have adapted the framework to ensure businesses receive further clarity on requirements with the intention of improving alignment. For example, the release of ‘core’ and ‘additional’ metrics will support the alignment of cross-sector metric reporting.

General Requirements

The TNFD has also set out six general requirements that cut across the four disclosure pillars. The TNFD has also set out six general requirements that cut across the four disclosure pillars. The general requirements consider varying levels of maturity, allowing report preparers to adapt their approach over time and increase the scope of disclosures.

The six general requirements relate to:

- The approach to materiality;

- The scope of disclosures made;

- Links between nature-related dependencies, impacts, risks and opportunities (referred to collectively in the TNFD framework as nature-related issues);

- The location specificity of nature-related issues;

- Integration with other sustainability-related disclosures; and

- Stakeholder engagement.

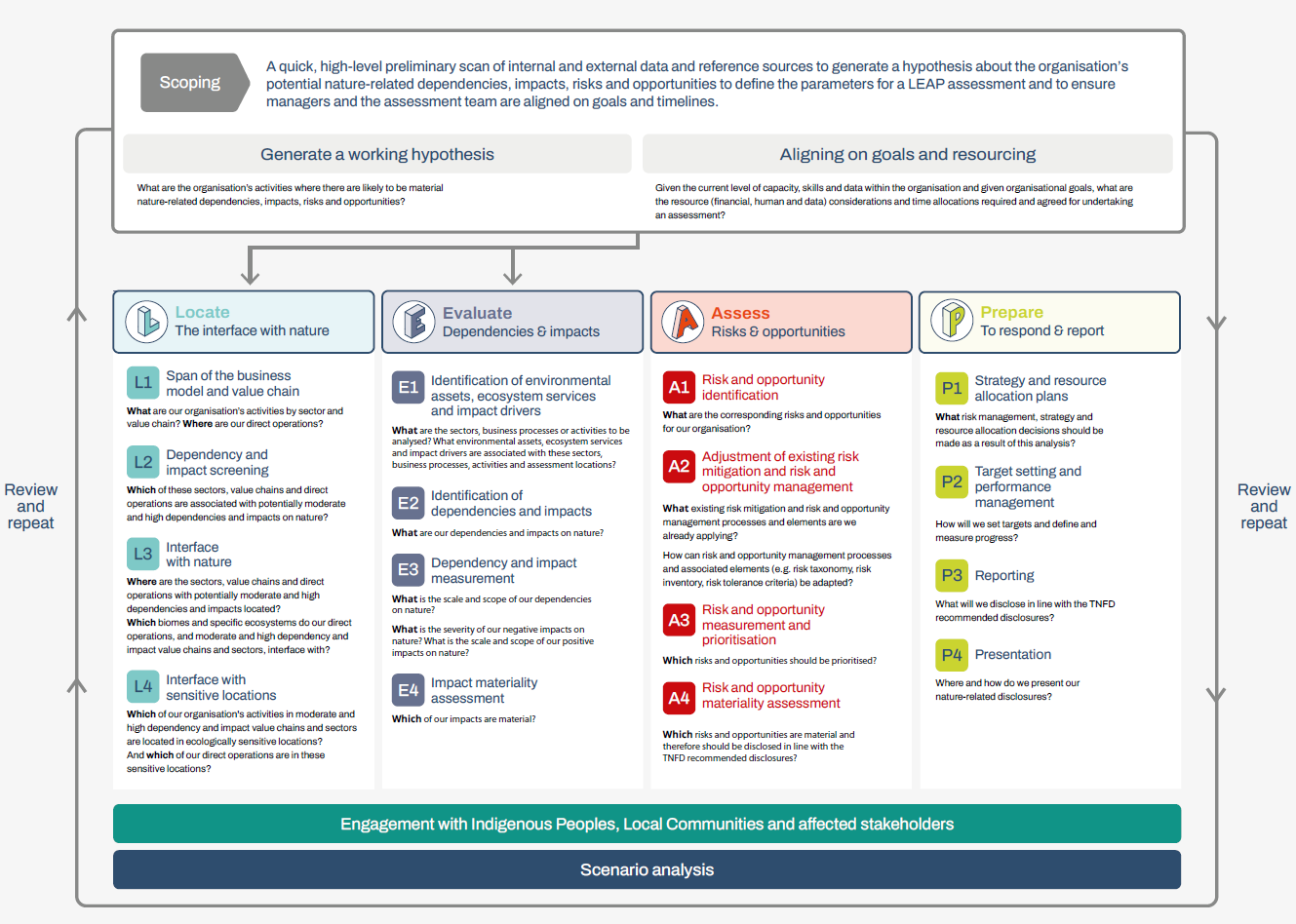

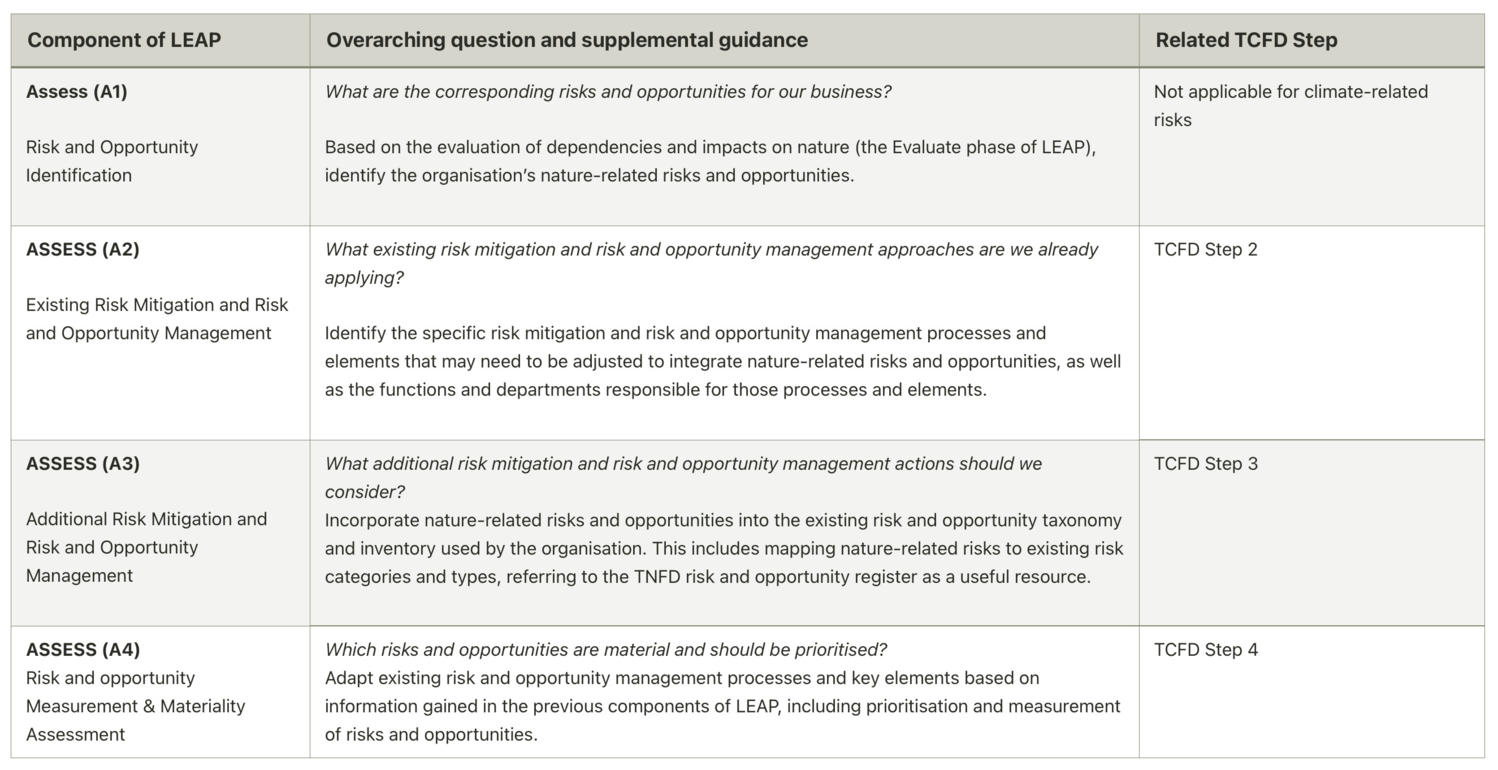

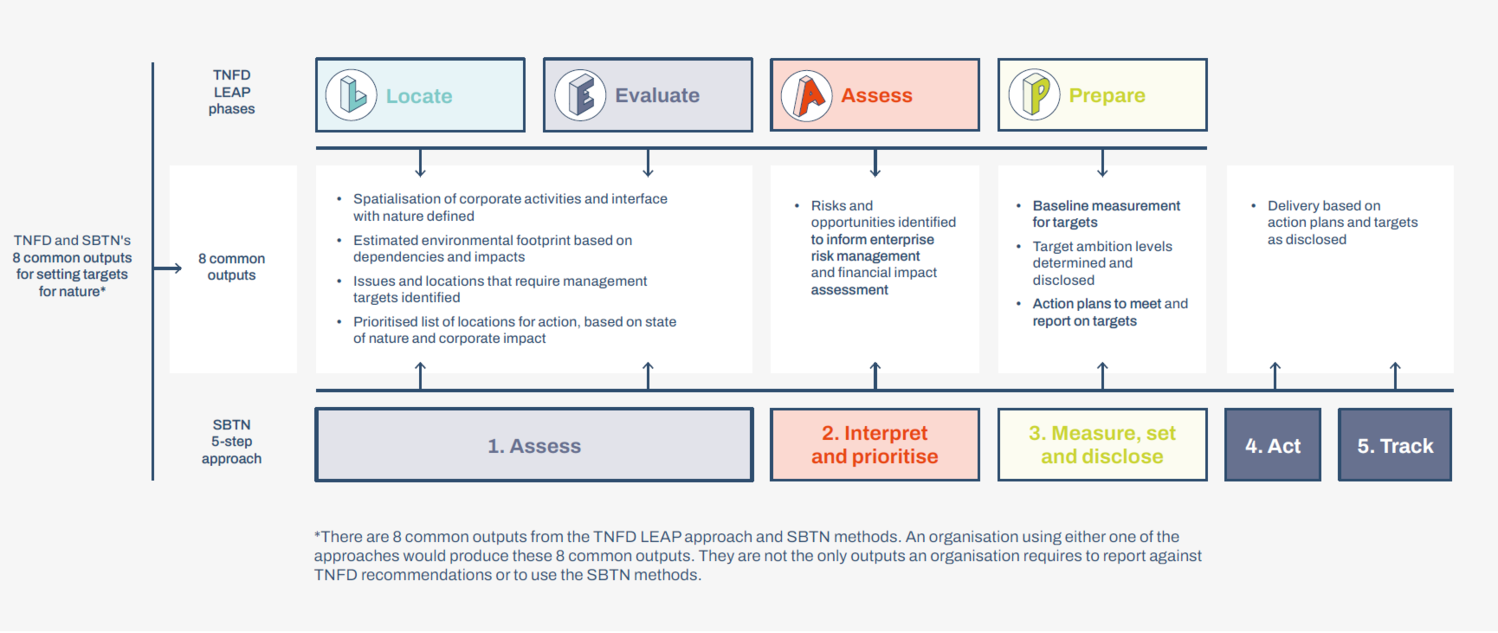

The LEAP approach

Along with the disclosure recommendations and general requirements, the TNFD has also created a voluntary process for assessing and managing DIROs called LEAP (“Locate, Evaluate, Assess, Prepare”).

Businesses may find that some of their existing practice and data collection aligns with TNFD’s LEAP approach. For examples from this pilot program, see the ‘Use cases’ section.

LEAP assessments are broken down into 16 analytic components, each framed by a guiding question. However, before commencing the LEAP assessment, the TNFD recommends reviewing the scope of the assessment in order to prioritize what is likely to be material for a business and to focus data collection. The scoping stage reflects the type of business, the different entry points into the LEAP approach and the varying types of analysis appropriate for each component of LEAP, with different framing questions for corporates vs financial institutions.

For specific guidance on scoping for different systems, see Roadmaps to Nature Positive: Foundations for Built Environment, Land use: agri-food (raw crops) and forest sectors, and Energy systems.

Figure 2: The TNFD approach for identification and assessment of nature-related issues – LEAP

Source: TNFD (2023). Guidance on the identification and assessment of nature-related issues: the LEAP approach. Retrieved here.

To understand the baseline of TNFD maturity at the start of the pilot, PwC conducted maturity assessments* against v0.2 of the framework. Pilot members’ public disclosures were reviewed and assessed against TNFD disclosure recommendations.

*Given the TNFD maturity assessments were conducted against v0.2 of the framework the results do not assess pilot members maturity against some of the TNFD’s recent recommendations (such as those regarding traceability and stakeholder engagement). The results are also based on disclosures from previous years which may have since been updated and improved. The maturity assessment findings highlight variability between systems based on the sample of 23 global businesses involved in this TNFD pilot).

Some key themes and topics applicable across all systems:

- Of the four phases of the LEAP approach, pilot members feel most confident in the Locate phase. However, pilot members found Locate more challenging for the downstream and upstream parts of the value chain with a lack of clarity around how to obtain location-specific data, especially in long and complex value chains.

- Of the four pillars of TNFD, pilot members feel most confident in governance. This is in part due to its similarity with TCFD and other reporting frameworks. Strategy is the pillar that presents the most difficulty, with nature-related scenario analysis being a very new area for companies that the majority of pilot members are yet to start tackling.

- Some quick wins identified by members included upskilling internal teams and mapping out existing data to understand what data from business operations and across the value chain is already being collected (for example, for climate disclosures).

Table 1: General learnings from PwC UK’s TNFD maturity assessments

Sector |

Existing alignment to TNFD |

Next steps for alignment |

Energy |

•Well established central •High TCFD maturity •High level nature positive commitments which consider Biodiversity, Water, Land use, atmosphere and resource efficiency |

•Disclose how nature-related risks and opportunities are identified, assessed, monitored and how these impact business strategy •Use risk categories (e.g., physical) and sub-categories (e.g., acute or chronic) to disaggregate lists of environmental risks, using short- (<2), medium- (2-5) or long-term (5+) time horizons where possible. •Set interim targets to support high level commitments e.g. “water positive”, “nature positive”, etc. •Link DIROs to financial implications |

Land Use |

•Case studies that highlight location-specific risks •Good TCFD structures which can be translated to TNFD, particularly around governance and risk management pillars •Clear nature strategies with associated high-level targets on nature |

•Improve description of board and management level responsibility for nature •Align to TNFD classification of risks i.e., physical, transition and systemic •Analyze value of nature-related dependencies, impacts, risks and opportunities in various nature scenarios •Set targets now and adapt them later, including KPIs to monitor progress |

Built Environment |

•Description of nature-related impacts influencing business planning •There is some discussion on how nature-related risks are being managed, particularly for water and waste •Good inclusion of stakeholders e.g. for materiality review •Nature is frequently thought •Clear targets for site level operations, with nature-related opportunities defined |

•Leverage TCFD learnings on risk classification, description of business opportunities etc. •Include diagrams that represent governance structures and risk management approaches to demonstrate how information is passed across the organization •Describe strategic decision-making implications •Develop a more holistic approach to nature, covering a range of concepts, realms, assets |

Getting started using the LEAP approach

Introduction

This section provides insights on implementing elements of the LEAP approach, collated by incorporating TNFD guidance and examples generated by pilot members, WBCSD and PwC during pilot workshops. Workshops focused on specific challenging aspects of the TNFD framework as identified during the maturity assessments and in collaboration with pilot members. Each challenge area relates to a different stage of the LEAP approach.

- Scoping: Scoping value-chain assessments

- Evaluate: Identifying and measuring dependencies

- Assess: Identifying and assessing risks and opportunities

- Assess (cont.): Nature-related scenarios

- Prepare: Target-setting

- Approaches used by Financial Institutions

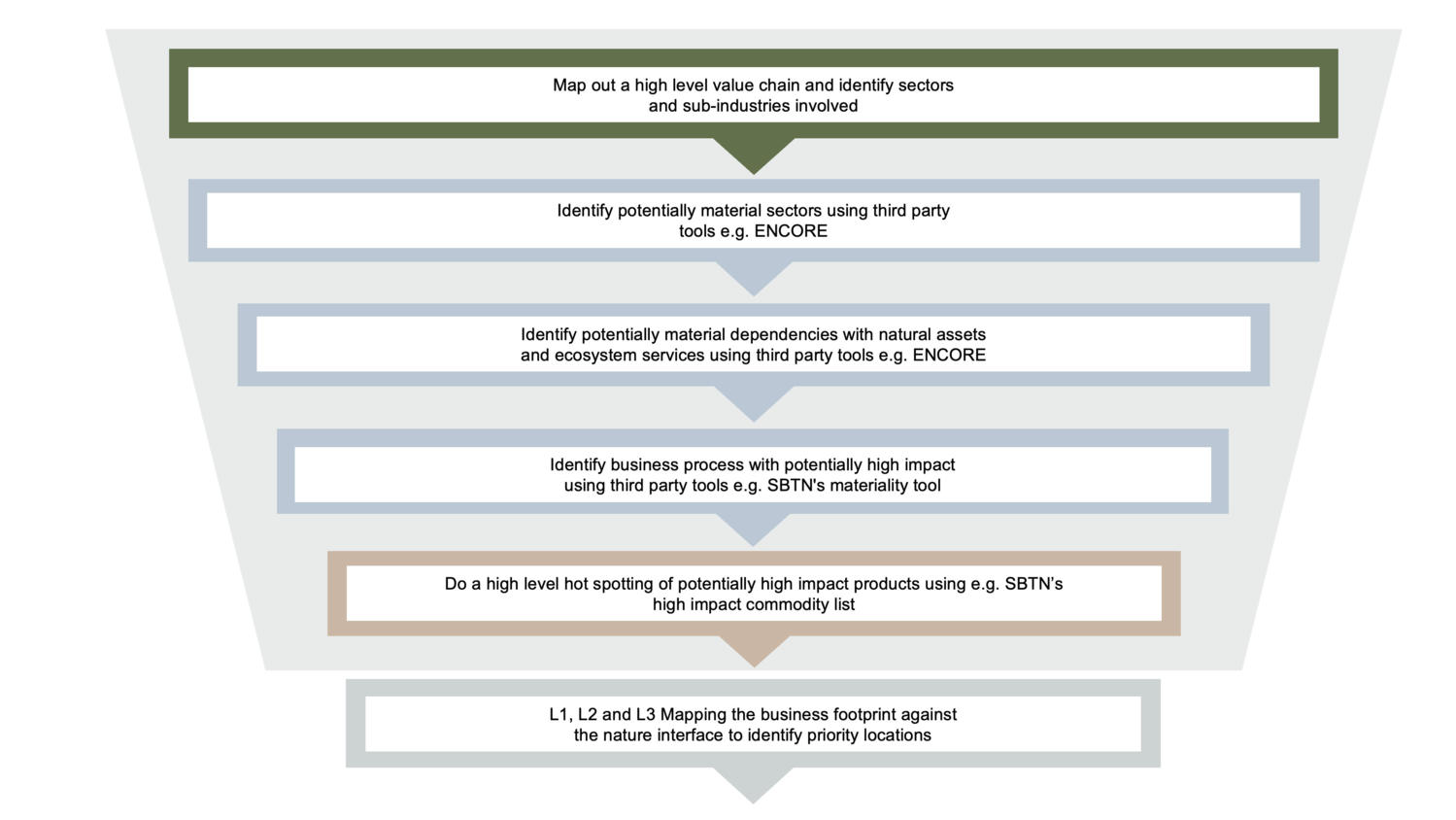

The 5-step approach to scoping LEAP assessments outlined below was adapted from TNFD v0.3 guidance by PwC and does not constitute direct TNFD guidance. Each step outlined below can be thought of in a funnel approach as depicted by the diagram in figure 3, which together can generate a working hypothesis to take into further LEAP assessments.

Table 2: PwC’s suggested 5 step approach to scoping LEAP assessments

Step |

Suggested approach |

||

1 |

Identify sectors present in the value chain |

Map out and assess the value chain components (e.g. suppliers, intermediaries, customers, etc.) to identify which sectors are involved. Consider where in the value chain the sector classification changes from one stage to another using sector classification systems such as Global Industry Classification Standard (“GICS”) (which is used for the ENCORE tool) or Sustainability Accounting Standards Board (“SASB”) (recommended by TNFD). |

|

2 |

Screen for potentially high risk sectors |

Of the sectors identified, use a high-level screening tool such as ENCORE to understand which sectors and sub-sectors are potentially high risk. This can be calculated in a variety of ways as long as the method is disclosed (e.g. aggregated ENCORE score across all impacts and dependencies multiplied by the scale and intensity of operations for each sector). |

|

3 |

Screen for where in |

Identify which natural assets and ecosystem services you are potentially highly dependent on in these sub-sectors. For example, using ENCORE to understand which production processes within each sub-industry have 'high' or 'very high' dependencies on the natural assets/ecosystem service. |

|

4 |

Screen for where in the value chain potential impacts might occur |

Which business processes have a potentially high impact on ecosystem services/natural assets (within the high risk sub-industries previously identified in part (1)). For example, use SBTN’s sectoral materiality tool to understand which production processes have ‘high’ or ‘very high’ impacts. |

|

5 |

Explore potentially high impact products |

Narrow the scope further based on the presence of any high impact commodities in the value chain which should be prioritized to explore in more detail. Potentially high impact commodities could be explored using SBTN’s high impact commodity list or tools such as TRASE. |

|

Figure 3: Visualization of the suggested approach to scoping LEAP assessments

This scoping approach provides a basis for businesses to understand potentially high impact or highly dependent parts of their business operations or wider value chain. These need to be explored in terms of financial magnitude, such as associated spend, cost or revenue data. In addition, TNFD suggests performing a high-level hotspotting.

Table 3: Built Environment members’ examples from the value chain (step 1 - Identify sectors present in the value chain)

Type of business |

Upstream |

Direct operations |

Downstream |

|||

Construction company |

Material extraction |

Transportation |

Construction |

Waste and demolition |

||

Construction materials manufacturer |

Procurement of raw materials |

Materials extraction and processing |

Transportation of materials |

Construction |

Waste and demolition |

|

For specific guidance on typical impacts and dependencies for different systems, see Roadmaps to Nature Positive, Land-use: agri-food (row crops) and forest sectors and, energy systems

Table 4: Built Environment members’ answers to steps 2, 3, 4 and 5 in the outline 5 step process

Potentially high risk sectors |

Potential dependencies |

Potentially high risk processes |

Potential Impacts |

Potentially high risk commodities |

Precious metals and materials |

Surface water |

Construction materials manufacturing |

Lowering water quality |

Steel |

Product provision |

Ground water |

Mining for materials |

Lowering of the water table |

Sand |

Landscaping/ |

Soil quality |

Construction |

GHG emissions |

Cement |

This process allows businesses to understand that water availability (as one example) is likely to be a material dependency in the Built Environment sector and therefore all water stressed areas where operations are occurring should be identified. Tools such as the Aqueduct water risk atlas can facilitate this analysis as part of the ‘Locate’ phase of LEAP.

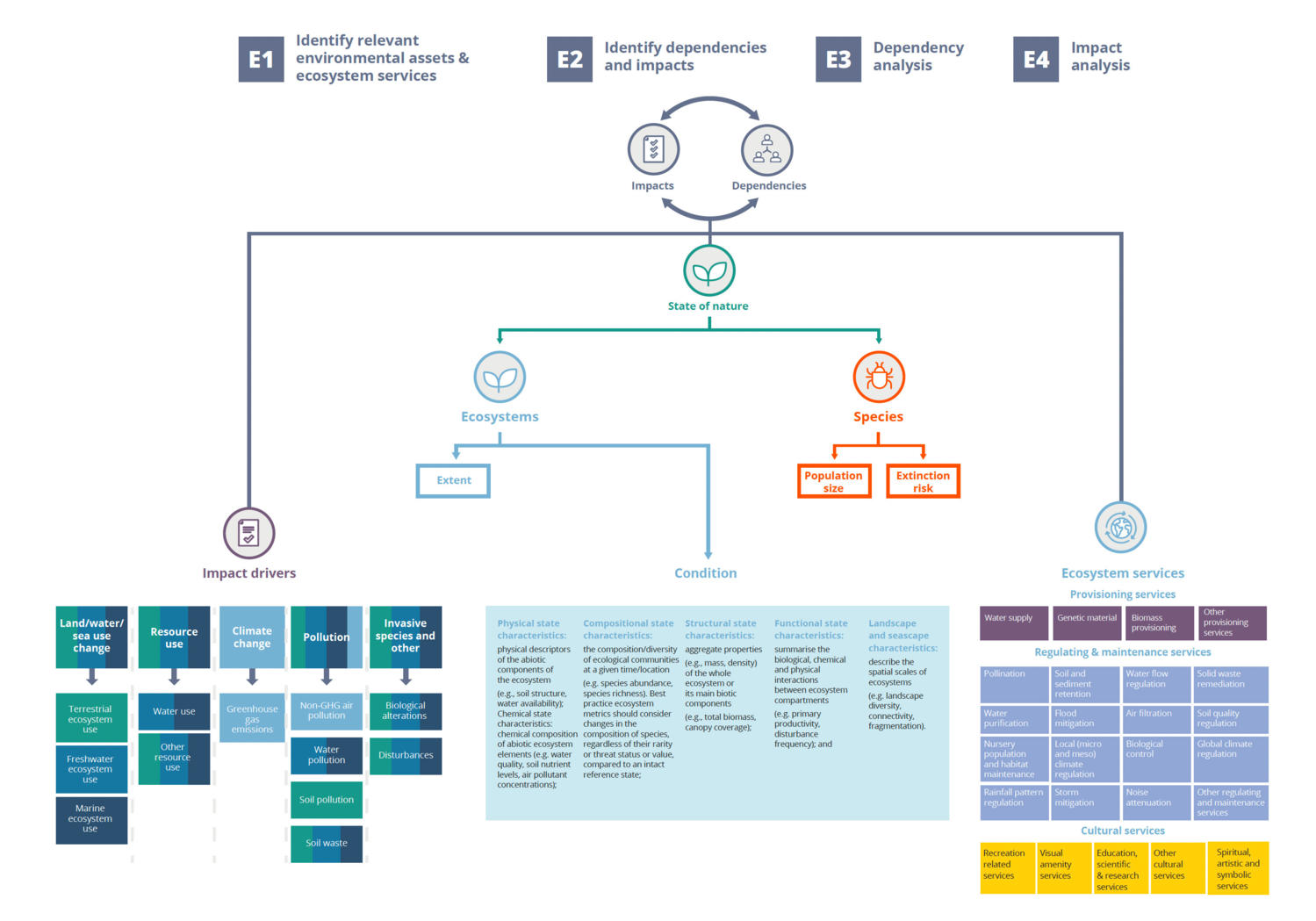

TNFD’s ‘Evaluate’ stage of LEAP is about identifying and analyzing impacts and dependencies (see here). TNFD defines impacts and dependencies on nature as follows_

Impacts: Changes in the state of nature, which may result in changes to the capacity of nature to provide social and economic functions. Impacts can be positive or negative. They can be the result of an organization’s or another party’s actions and can be direct, indirect or cumulative.

Dependencies: Aspects of ecosystem services that an organization or other actor relies on to function. Dependencies include ecosystems' ability to regulate water flow, water quality, and hazards like fires and floods; provide a suitable habitat for pollinators (who in turn provide a service directly to economies), and sequester carbon (in terrestrial, freshwater and marine realms).

Figure 4: Deep dive into the evaluate phase of the LEAP approach, focusing on impacts and dependencies, included in TNFD v0.4.

A list of potential dependencies for each sector was taken from the ENCORE platform. In order to assist identification of additional dependencies, other tools used by members were identified.

Tools/methods used by members to support identification and evaluation of dependencies

- Guidance. TCFD, ENCORE, Food, Land and Agriculture Guidance (“FLAG”) from the Science-based Targets Initiative or “SBTi”, GLOBIO, guidance from accepted certification standards, WWF Biodiversity Risk Filter and SBTN helped corporates to define scope and method for dependency analysis.

- Tailor made tools. One example was the use of Integrated Biodiversity Assessment Tool (“IBAT”), in conjunction additional Geographic Information System (“GIS”) layers representing different ecosystem services, to show the footprint of potential dependencies for the organization.

- Primary data inputs. Data already being collected by the business regarding usage or consumption can help to identify nature-related dependencies based on an understanding of the linkages between production and dependencies. For example, water consumption from local water bodies or use of land for growing crops.

- Third party geospatial tools. Geographical mapping of assets/operations (including value chain operations where possible) in relation to nature-related risk(s). For example, the mapping of water risk using Aqueduct.

- Stakeholder workshops. Methods identified to help the process of qualitatively evaluating the materiality of identified dependencies. For example, a pilot member suggested creating a spreadsheet to list out different dependencies, how likely they are to occur and potential strategic responses based on workshops and discussions held with key stakeholders.

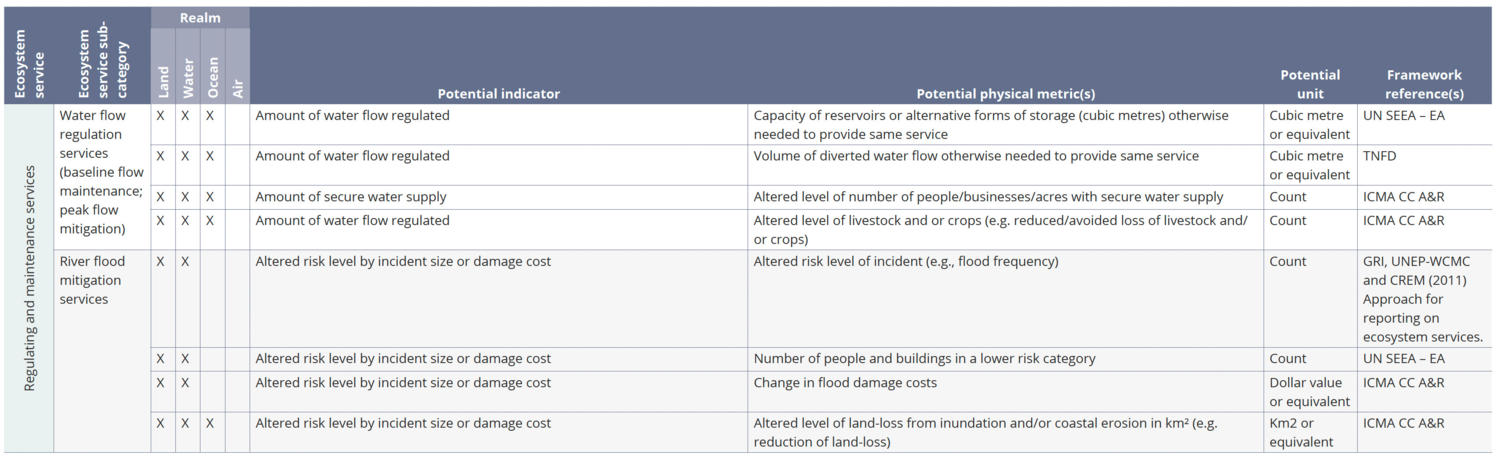

Dependencies and their related metrics

The TNFD provides an extensive table of ecosystem services and potential physical metrics, which could be used to measure potential ecosystem indicators for each (see Figure 5).

Figure 5: Example of ecosystem service metrics

Source: TNFD (2023). Guidance for corporates on science-based targets for nature, Annex 1. Accessible here.

This allows businesses to understand the extent of their dependency on ecosystem services and conclude which are most material to their business. They should then be prioritized when considering risk and impact management or making strategic decisions. An example of a dependency identified as potentially material for each sector is highlighted in table 5 below, along with the potential ecosystem indicators, metrics and data sources to measure each one.

Table 5: Dependencies and their related metrics

System |

Example dependency |

Example ecosystem indicator |

Example metric |

Example data source |

Energy |

Surface water availability |

Water consumption |

Volume of water consumption by source (m3) |

Consumption data |

Land use |

Soil quality |

Soil Organic Carbon (SOC) level |

SOC reported as a percentage of topsoil and converted to volume per hectare (t/ha) |

Supplier land use data |

|

Built Environment

|

Timber (upstream) |

Carbon balance related to timber (i.e. net carbon emissions and storage) |

Volume of timber used that was sustainably harvested/produced |

Data collected |

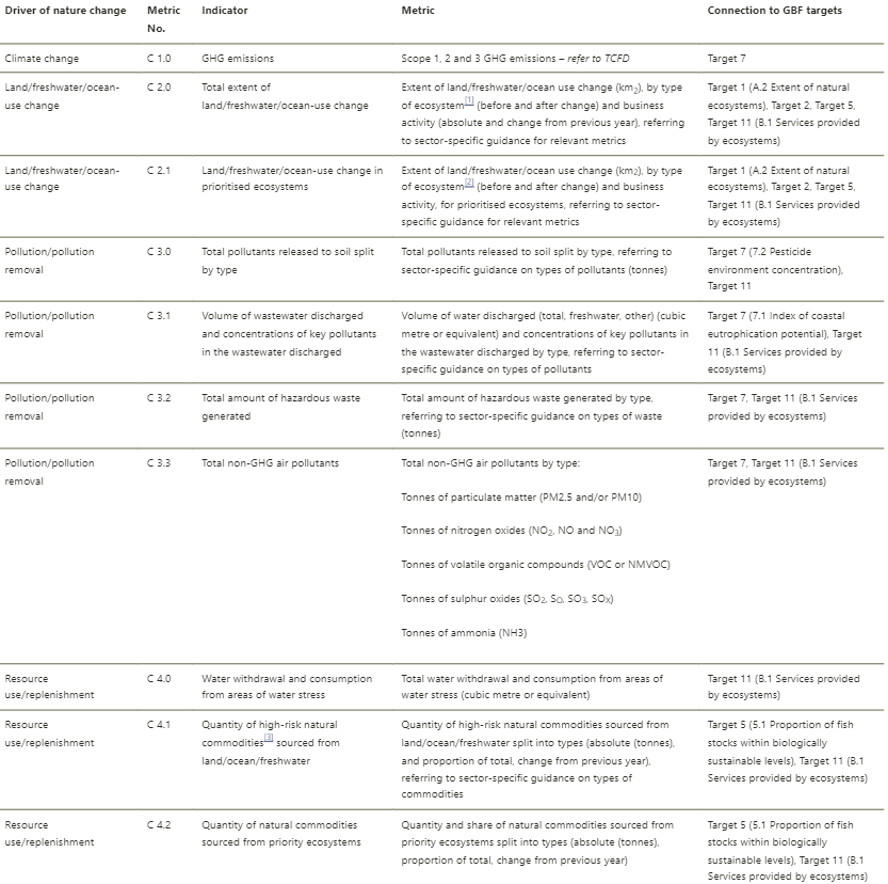

The TNFD recommends 10 ‘core’ metrics which should be disclosed against ‘Metrics and Targets B’ and ‘Strategy A’, with relation to a business’ dependencies and impacts on nature. These ‘core’ metrics are aligned to global policies such as the Global Biodiversity Framework (GBF) and therefore the TNFD encourages businesses to disclose against all of the metrics that are relevant to the business model, sector(s), biome(s) and priority locations.

Further considerations regarding the ‘core’ metrics include:

- the measurement baseline, for example, the percentage change from previous reporting years

- direct operations should be disclosed separately from upstream, downstream or financed activities (in the case of FIs)

- state the location the metric refers to

- consider disclosure of these metrics alongside TNFD disclosure guidance for ‘Metrics and Targets B’ and ‘Strategy A’

- for impact drivers, organizations should ensure the metric enables report users to determine what the impact driver is (e.g. the type of pollutant emitted), where the impact is located, with reference to spatial data where possible and how much impact has taken place (e.g. the volume of pollutant emitted).

If organizations do not report against any of the core metrics, they should provide an explanatory statement as to why they have not reported.

Figure 6: ‘Core’ disclosure metrics for dependencies and impacts on nature

Source: TNFD (2023). Guidance on the identification and assessment of nature-related issues: the LEAP approach. Retrieved here. Please access the full TNFD Pilot report for a closer look at this figure, p.16-20.

For specific guidance on typical impacts and dependencies for different systems, see Roadmaps to Nature Positive, Foundations for Built environment, Land-use: agri-food (row crops) and forest sectors and , Energy systems

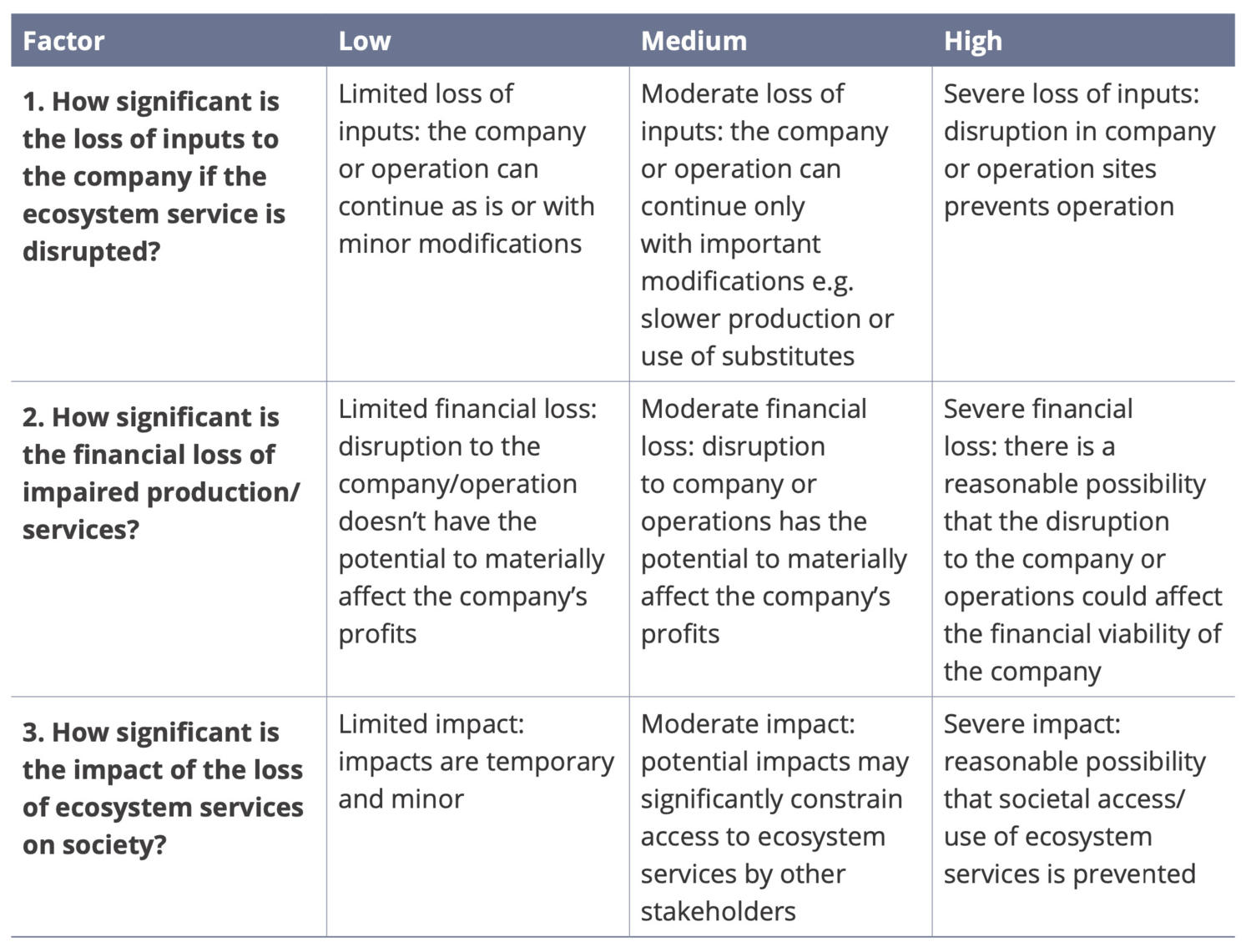

To evaluate key dependencies, TNFD recommends consideration of factors related to dependency materiality assessment and provides some examples (see here).

Figure 7: Criteria for identifying potentially significant ecosystem services

Source: TNFD (2023). Guidance on the identification and assessment of nature-related issues: the LEAP approach. Retrieved here.

TNFD suggests that any additional materiality factors should be those already used in materiality assessments elsewhere in the organization. TNFD allows organizations to choose their approach to materiality, rather than endorse one approach to materiality over another. For example, ‘double materiality’ or ‘dynamic materiality’ may be chosen based on regulatory requirements or reporting and disclosure preferences. This supports alignment with the emerging global baseline currently under development by the ISSB .

Examples of materiality factors being used by pilot members

- Capacity of the business to influence or change the natural environment they impact / are dependent upon.

- Business criticality, for example, using volumetric data on raw materials by country and region, or spend-based data on suppliers.

- Stakeholders materiality assessment (internal and external) with quantitative targets.

Following the impacts and dependencies identified and evaluated in the ‘Evaluate’ phase of LEAP, the TNFD suggests overarching questions and supplemental guidance for the ‘Assess’ phase of LEAP (see here).

Figure 8: Overarching questions and guidance of the Assess phase of LEAP; and its relation to TCFD.

Source: TNFD (2022) TNFD Framework Beta v0.3. Annex 3.1: Guidance on the Assess Phase of LEAP. Retrieved here.

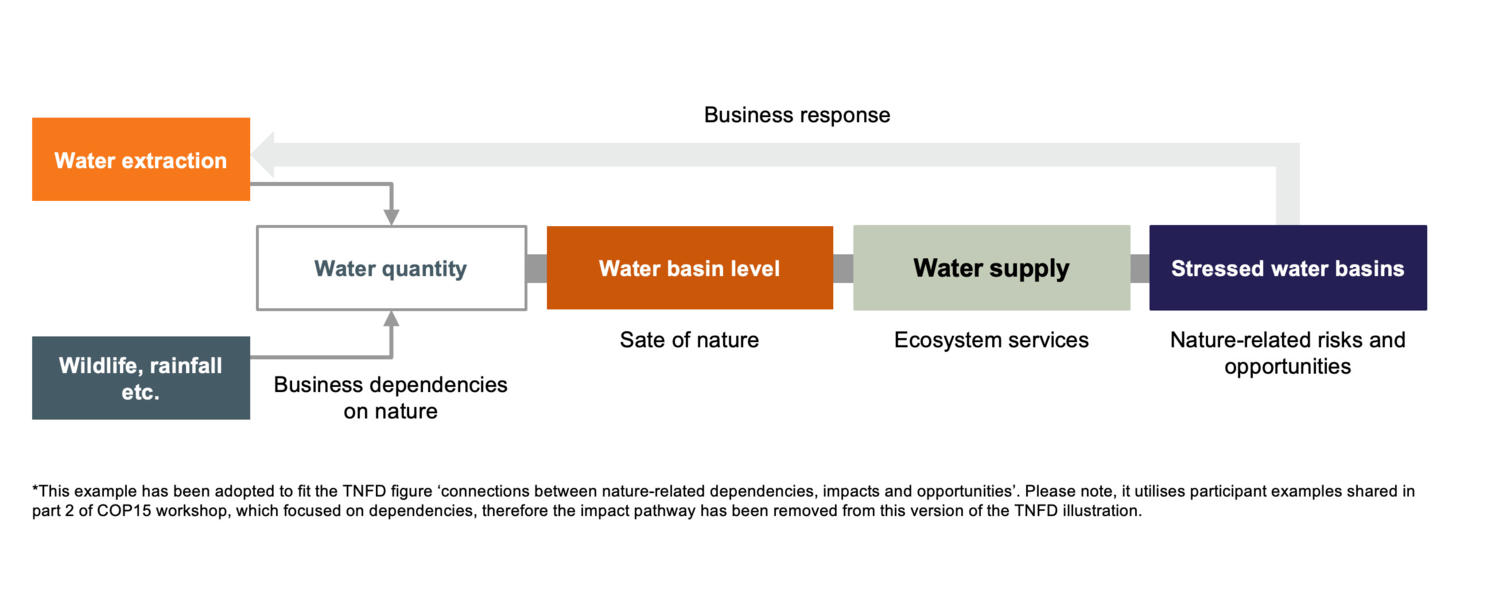

TNFD provides an example of a pathway for identifying risks based on impact drivers or dependencies (see here). Using an example impact driver (water extraction) and an example dependency (water quantity available for extraction) identified as material, the diagram below shows how this information can help to identify nature-related risks and opportunities (“R&Os”). In this instance, a highly stressed water basin, which is unable to meet water demand.

Figure 9: Example of a Risks and Opportunities identification pathway

Based on the risks and opportunities identified by following the TNFD’s pathway from identified impacts and dependencies, some examples of additional processes followed to identify nature-related risks and opportunities are outlined below.

For specific guidance on typical risks and opportunities for different systems, see Roadmaps to Nature Positive, Foundations for Built environment, Land-use: agri-food (row crops) and forest sectors, and energy systems.

Processes for identifying nature-related risks and opportunities

- Third party geospatial tools. For example, STAR, WWF Risk Filter Suite and Aqueduct.

- Third party methodologies and decision-making tools. For example, The Corporate Ecosystem Services Review provides a methodology to help identify and assess risks and opportunities.

- Internal tools. Readily available technologies which can be leveraged such as geospatial analysis for farmland or timberland properties.

- Additional guidance. The most cited guidance was SBTN guidance and the IUCN standards.

- Existing risk screening processes. Screening processes that capture risks at a more generalized level which might include nature-related risks. These processes may need to be reviewed and refined if existing enterprise risk management (ERM) processes do not take nature positive strategies into account.

- Local/site level environmental assessments. For example, surveys to collect relevant, granular data might reveal significant changes in natural capital.

- Existing risks. An organization’s internal risk register is likely to have previously captured risks, which are related to nature. For example, water-related risks if there is a significant presence in a water-stressed area.

- Existing opportunities. Opportunities previously captured related to nature. For example, conservation and restoration of important habitats, or implementation of nature-based solutions.

Once the potential risks and opportunities have been identified, these can be used to populate the TNFD’s template R&O register (see here).

Figure 10: TNFD’s example Nature-related Risk Register

Source: TNFD (2022). Risk and Opportunity Registers. Retrieved here.

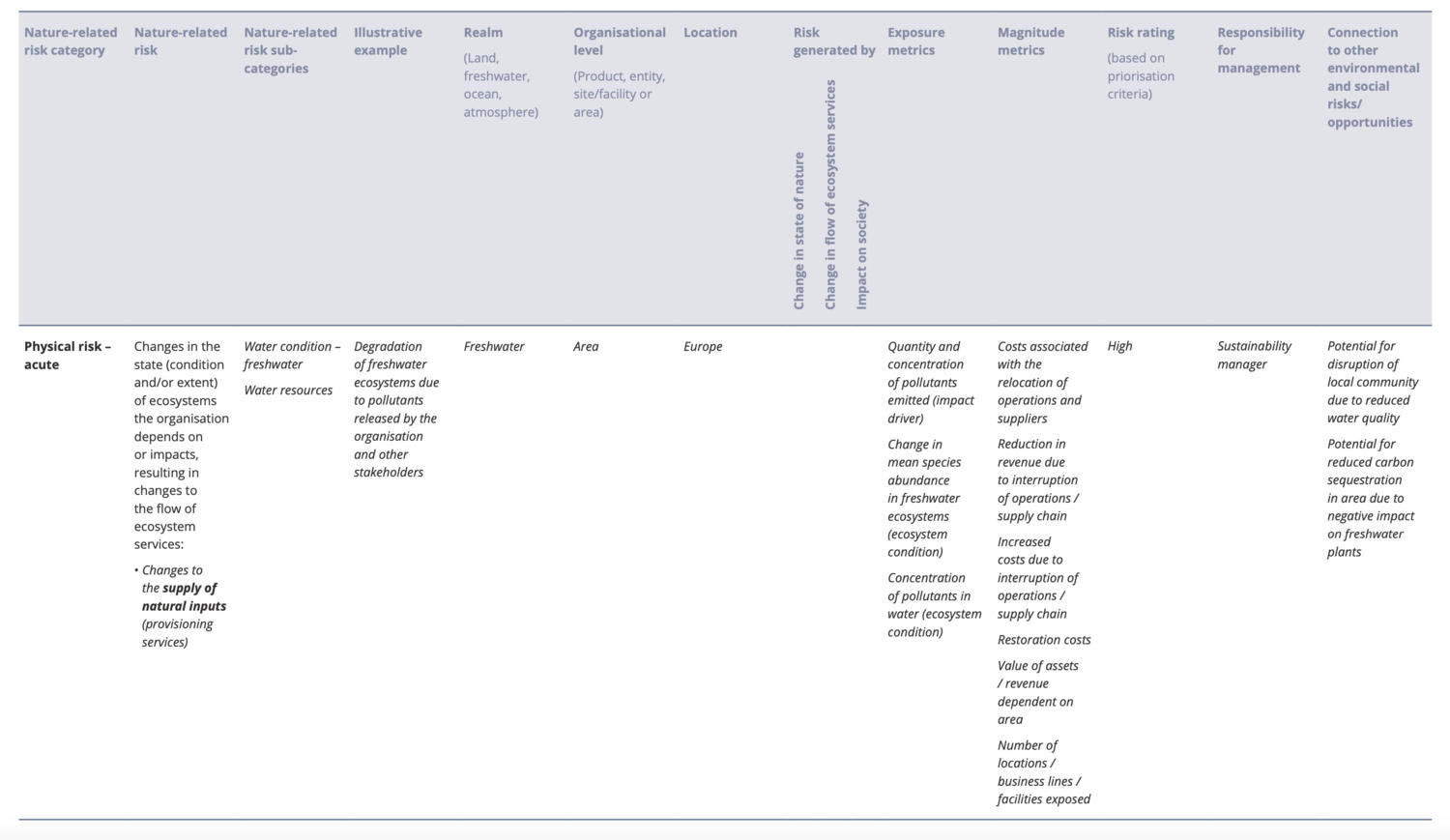

An example of what this risk and opportunity register might look like in practice for ‘loss of forest resources due to increasing fires’ can be seen below. The TNFD suggests potential metrics to measure exposure and magnitude, which can be utilized to determine materiality of each risk/opportunity (see full list here).

Table 6: Land Use members’ example risk and opportunity register

Risk Registry Category |

Example Response |

Type of risk/opportunity |

Physical – chronic |

Illustrative example |

Loss of forest resources due to increasing wildfires |

Realm |

Land |

Organizational level |

Product |

Location |

Worldwide |

Risk generated by |

Change in state of nature |

Exposure metrics |

|

Magnitude metrics |

|

Risk rating |

4 – Very high |

Responsibility for management |

Site level operations |

Connection to other environmental |

|

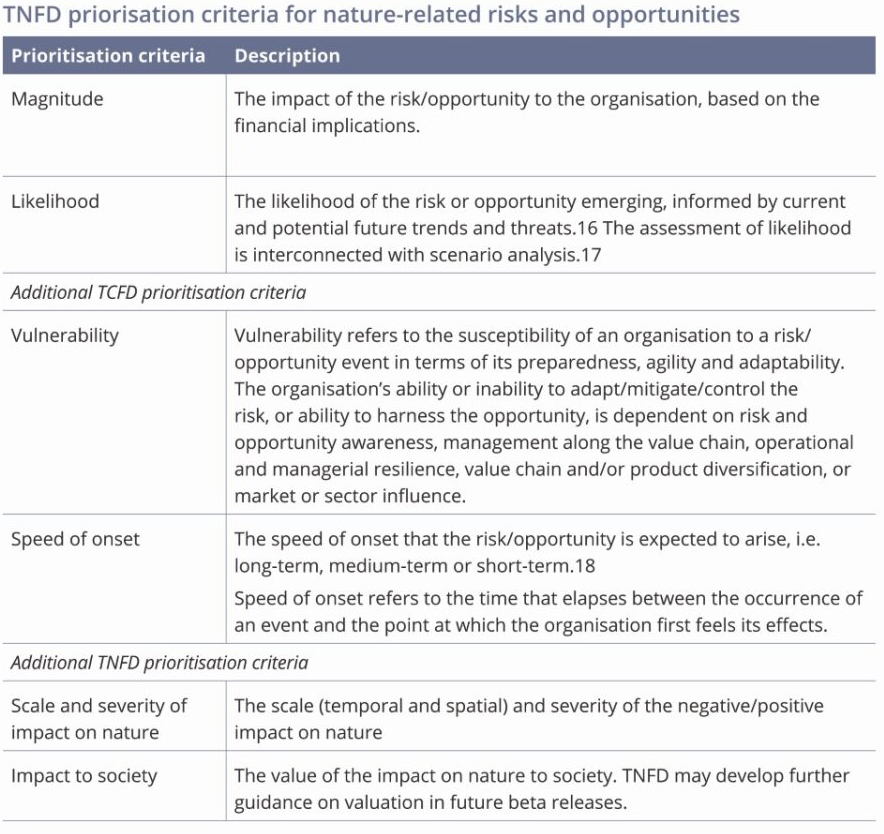

Following identification of magnitude and exposure metrics, the TNFD recommends exploring any additional prioritization criteria that might be relevant to your organization (see here).

Figure 11: TNFD’s prioritization criteria for nature-related risks and opportunities

Source: TNFD (2023). Guidance on the identification and assessment of nature-related issues: the LEAP approach. Retrieved here.

Examples of additional prioritization criteria

Some examples of additional prioritization criteria are provided below.

- Opportunity for positive impact. The size of the opportunity to reverse the negative risk into a positive impact. For example, any opportunities for realizing co-benefits such as carbon sequestration.

- Ease of risk mitigation. Risks that have an easy solution (technically, financially etc.) would be less material.

- Social aspects of the risk’s location. For example, in countries with less strict regulations, the risk may be more material.

It is important to note that as corporate maturity on nature increases over time, expectations both internally and externally increase to understand the materiality of each risk/opportunity under different nature-related scenarios. This nature scenario exploration will build on existing climate scenarios work such as WBCSD’s Energy Scenario Catalog and Food & Ag Scenario Explorer to incorporate nature-related factors.

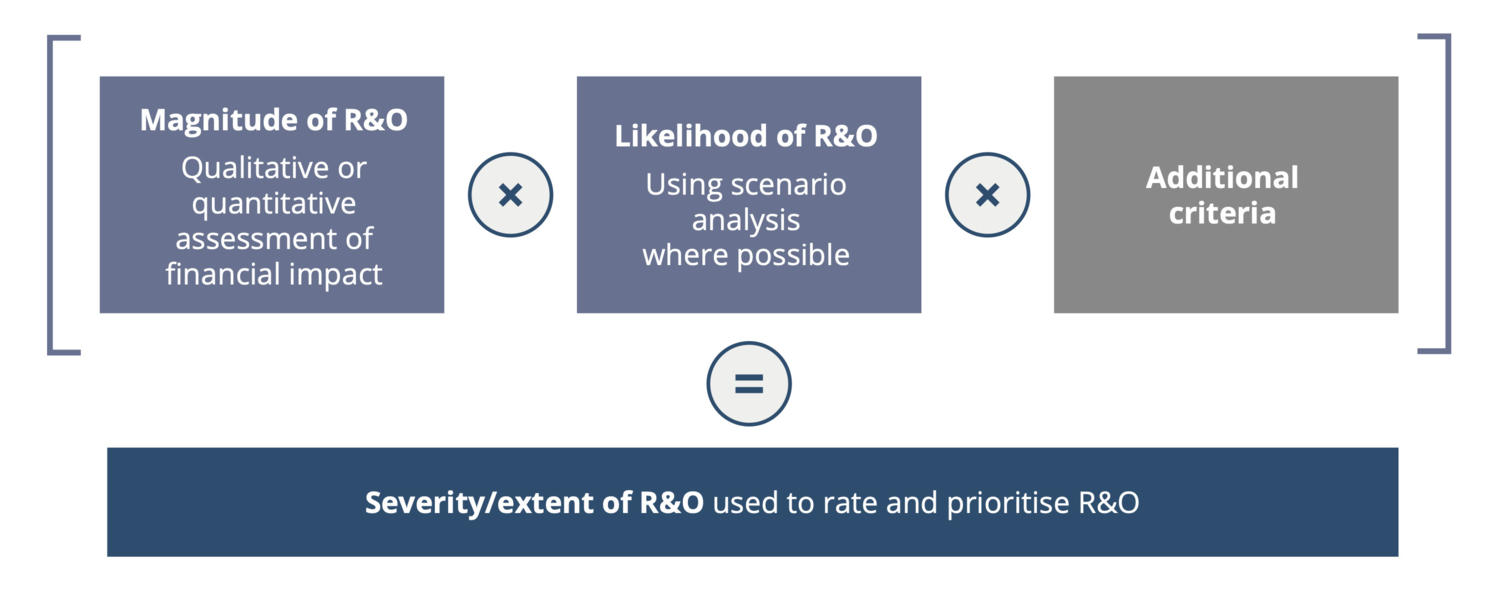

Following identification of all relevant prioritization criteria, each nature-related risk/opportunity identified should be scored against magnitude, likelihood (exposure) as well as any other relevant criteria (see here).

Figure 12: Criteria for prioritizing nature-related risks and opportunities

Source: TNFD (2022) TNFD Framework Annex 3. Retrieved here.

The multiplication of these factors will allow prioritization of each R&O, with those scoring highest being the most material (see here).

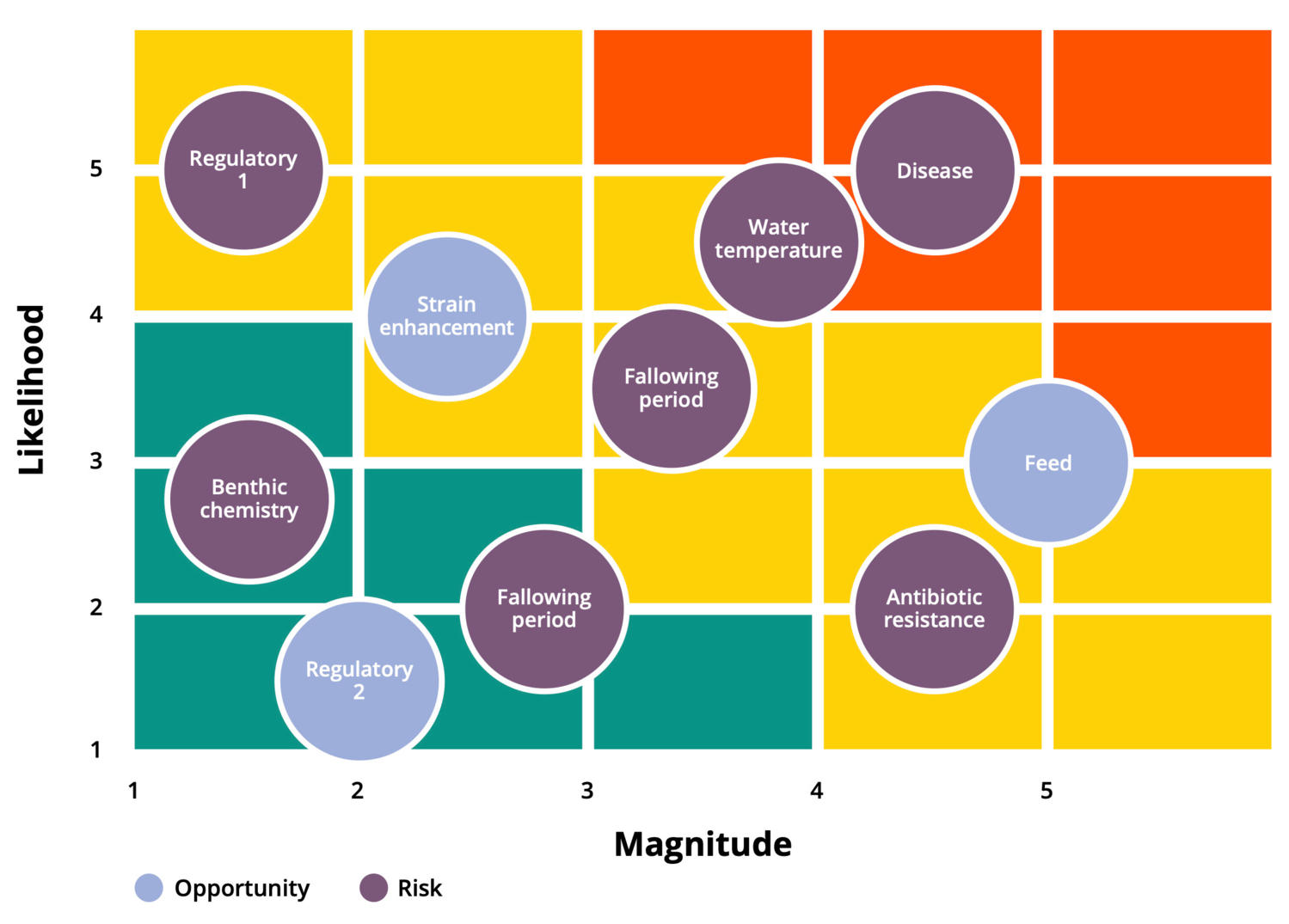

Figure 13: Example from TNFD’s Aquaculture case study on risks and opportunities

Source: TNFD (2022). TNFD aquaculture case study. Retrieved here.

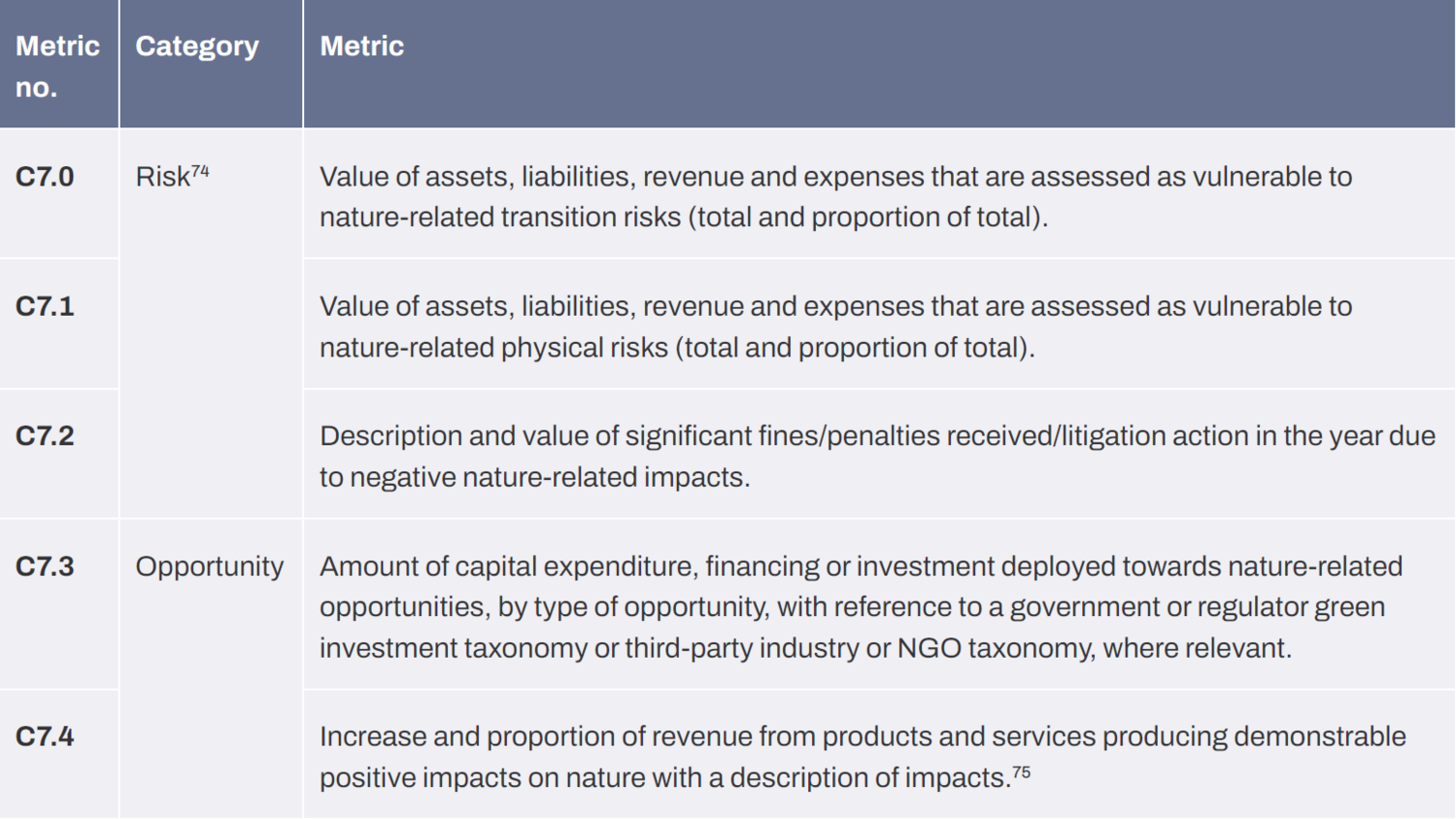

The TNFD provides guidance on ‘core’ risk and opportunity metrics that should be included in disclosures (see here). These metrics support TNFD disclosures against ‘Metrics and Targets A’, ‘Strategy A’ and ‘Strategy B’. If businesses do not report against any of the metrics listed in figure 14, they should provide an explanatory statement as to why they have not reported.

Figure 14: TNFD core global disclosure indicators and metrics for nature-related risks and opportunities

Source: TNFD (2023). Taskforce on Nature-related Financial Disclosures (TNFD) Recommendations. Retrieved here.

There are also ‘additional’ risk and opportunity metrics that can help guide the business on their most material risks and opportunities, for optional disclosure.

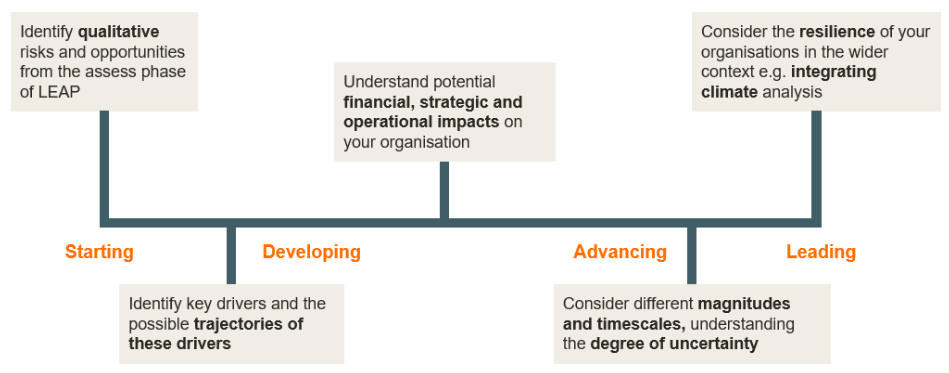

Nature-related scenario analysis is complex and should be viewed as a journey with businesses increasing in maturity over time. TNFD specifies the importance of understanding the world in which the business may have to operate, before making any decisions. As part of the pilot, a maturity scale was developed based on TNFD v0.4 guidance to show a suggested pathway for companies to move from qualitative risk and opportunity assessment all the way to quantitative analysis that considers financial, strategic and operational impacts as well as resilience.

Approach to scenario analysis maturity assessment

Figure 15: Illustrative scenario maturity steps

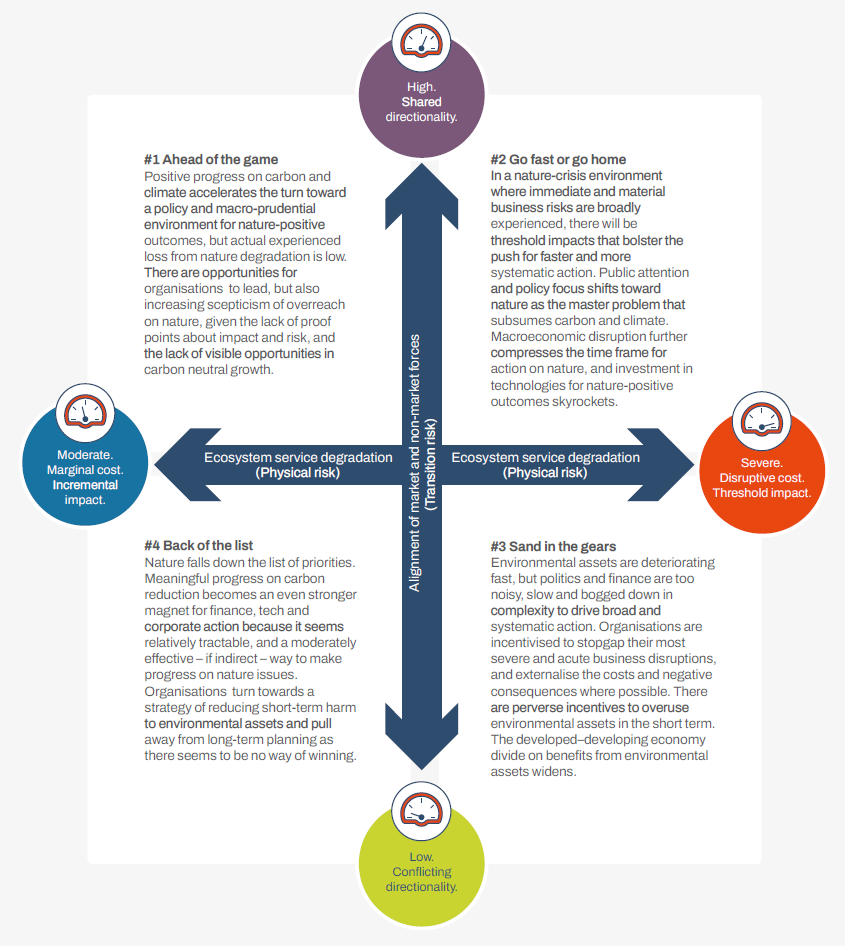

To identify risks and opportunities and inform strategy thinking, TNFD recommends initial qualitative exploration of “what if” scenarios following its 2x2 scenario frame . For example, by exploring the TNFD scenario ‘#2 Go fast or go home’ businesses can understand how they might operate in a future where there is ‘High ecosystem degradation’ but also ‘High alignment of market and non-market forces’, which form the two axes of TNFD ‘uncertainty axes’ (see figure 16).

The TNFD outlines a 4 step approach (see here), that businesses can follow for further exploration of each scenario. Below we have outlined some practical suggestions following these steps, including the development of financial impact pathways.

Figure 16: TNFD’s default nature-risk scenarios

Source: TNFD (2023). Guidance on scenario analysis. Retrieved here.

Figure 17: TNFD’s Step-by-step approach to scenario analysis

Source: TNFD (2023). Guidance on scenario analysis. Retrieved here.

Scenario Analysis step 1: Identifying the relevant driving forces

Step 1 involves identifying relevant driving forces for the scenario being explored. A description of driving forces relevant for TNFD’s scenario #2 is included below.

Table 7: A description of each of the driving forces in TNFD’s scenario #2 for High Ecosystem service degradation

Driving Forces |

High Ecosystem Service Degradation |

Local ecosystem and asset interactions, dependencies and impacts |

Nature-crisis where immediate and material business harms are broadly experienced |

Table 8: A description of each of the driving forces in TNFD’s scenario #2 for High Alignment of Market and Non-market Driving Forces.

Driving Forces |

High Alignment of Market and Non-market Driving Forces |

Regulators, legal and policy regimes |

Faster and more systematic action |

Stakeholder and customer demands |

Public attention and policy focus shifts towards nature |

Direct interaction with climate |

Nature subsumes carbon and climate |

Macro and micro economy |

Macroeconomic disruption reduces time for action |

Finance and insurance/Relevant technology and science |

Investment in nature related technologies skyrockets |

Scenario Analysis step 2: Placing the business or facility along the uncertainty axes

Step 2 suggests placing the business along the ‘uncertainty axes’ (see scenarios quadrant above), which provides an opportunity to include a variety of stakeholder perspectives to consider what the current and expected state of the business is for each specified future. For example, prompting questions can be discussed such as ‘where does the business sit along the uncertainty axes with respect to ecosystem service degradation?’ or ‘where does the business sit along the uncertainty axes with respect to alignment of market and non-market driving forces?

Scenario Analysis step 3: Using scenario storyline descriptions

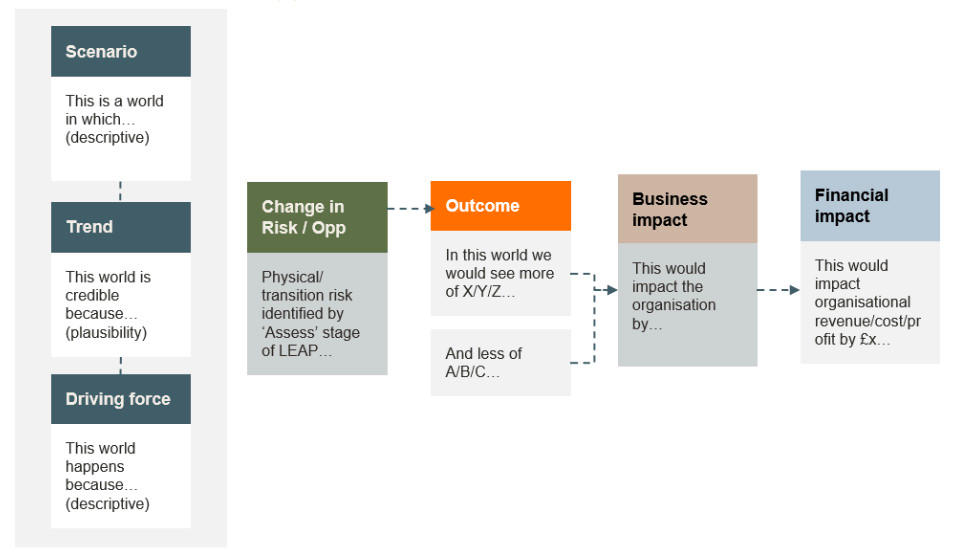

Step 3 prompts businesses to think about what new risks and opportunities would emerge in each of the scenarios identified. As part of step 3 it is important to consider the financial impact pathway for identified risks (and opportunities) in the context of the trends and driving forces within that scenario. Companies can use scenario impact pathways to explore the potential effects of risks and opportunities under different future states.

Figure 18: Generic impact pathway used to track business and financial impacts of different scenarios, trends and driving forces.

Through exploring an example of a nature-related risk, in this instance the ‘increased incidence in drought conditions and water shortages’, the example below shows how a risk can be translated into a potential financial impact for a business under the ‘#2 Go fast or go home’ TNFD scenario.

Figure 19: Impact pathway used to track business and financial impacts of an increased incidence of drought conditions and water shortages scenario

Further sector-specific examples of financial impact pathways relevant to the ‘#2 Go fast or go home’ scenario are detailed below.

Table 9: Impact pathways for different systems used to track business and financial impacts of different changes in risks and opportunities

Sector |

Change in risk or opportunity |

Outcome: The direct consequence of the risk if it materializes |

Business Impact: How does the outcome affect business activities and operations? |

Financial Impact: What’s the impact on cost, savings, revenue and financial performance? |

Energy |

Transition to processes with reduced negative impacts on nature/ increased positive impacts |

Example risk: Difficult to build new sites/increase capacity if placed in high biodiversity areas. |

Not achieving business targets at company level or even national level (European RES targets, for example). |

Increased liability costs and blocked revenues from non finalized projects. |

Example opportunity: Solar farm plans include co-creation of suitable habitats that encourage pollinators and provide connectivity corridors. |

Local community acceptance of the proposed projects, faster approvals |

Increased revenue. |

||

Land Use |

Increased demand/

|

Example risk: Prices increase for plant based inputs for agriculture e.g. seeds, biologicals and animal feed. |

Increased operational costs lead to increased cost of goods/products e.g. animal protein. |

Higher prices reduce attractiveness of the market, therefore reducing revenue. |

Example opportunity: Restoration of degraded land for plantations. |

Improve local communities and customers perceptions whilst meeting customer demand for products. |

Increase in revenue as a result of increase in products and enhanced consumer sentiment. |

||

Built Environment |

Shifting consumer preferences to products with lower impacts on nature |

Example risk: Customers don’t want to buy as much cement as previously due to its high impact on water consumption. |

Reduced sales |

Reduced revenue. |

Example opportunity: Progressive rehabilitation on quarries. |

Improved image of company, positive stakeholder sentiment. |

More access to investor capital and increased land expansion approvals. |

Step 4: Identifying high-level business decisions

Following identification of the possible implications of each plausible future scenario, step 4 encourages businesses to discuss how this might:

- Inform medium to long-term decision making about governance, strategy, risk and impact management, targets and capital allocation

- Surface key insights about potential changes that could make the organization’s core business model and processes more resilient to climate change and nature loss

- Identify new business models, such as nature-based solutions, that are aligned with net zero and nature-positive goals and societal outcomes

- Determine what the company would disclose in line with TNFD’s Strategy C disclosure:

- ‘Describe the resilience of the organization’s strategy to nature-related risks and opportunities, taking into consideration different scenarios’

TNFD has various scoping questions, which can help guide companies through the 4-step process, for example:

‘What are the new business goals and opportunities that would be relevant/would need to be abandoned in this context?’

It is crucial to engage key stakeholders in this step, ensuring a diverse range of expertise from different parts of the organizations, such as legal, corporate, regulations, sustainability and commercial, to enrich the conversation.

Scenario analysis will help businesses to engage with investors on how and why they are scoping their nature-related assessment, for example, focusing on specific commodities or locations.

It will also help to anticipate views from different stakeholders, ranging from investors to the public, by answering the double materiality question “what is the potential risk nature poses to my business and what risk does my business pose to nature?”

For specific guidance on priority business actions for different systems, see Roadmaps to Nature Positive, Foundations for agri-food, Foundations for Built environment, Land-use: agri-food (row crops) and forest sectors and, Energy systems

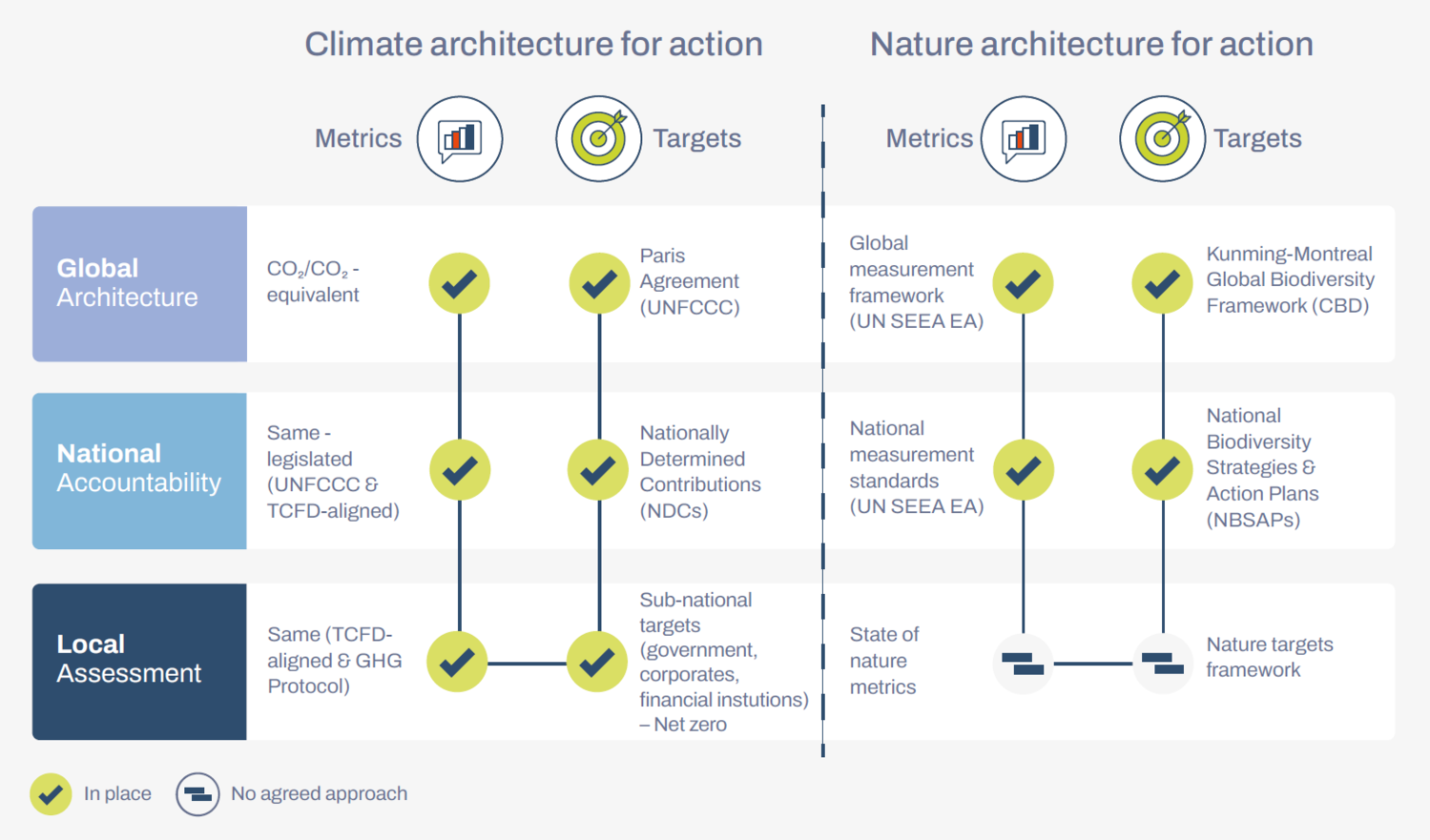

TNFD provides an architecture to help companies frame their targets. This suggests that businesses should utilize different measurement frameworks for targets depending on whether they were set at the Global, National or Local level (see here).

Figure 20: The architecture for measurement and target setting – Climate and nature

Source: TNFD (2023). Taskforce on Nature-related Financial Disclosures (TNFD) Recommendations. Retrieved here.

The TNFD has aligned its guidance with other global initiatives such as the SBTN target setting guidance (see here).

Figure 21: TNFD and SBTN fundamental areas of alignment on target setting

Source: TNFD (2023). Guidance for corporates on science-based targets for nature. Retrieved here.

Examples of global and local targets for businesses across each sector are displayed below, however, national targets are lacking. Many countries are still developing targets as part of revisions to National Biodiversity Strategies and Action Plans (“NSBAPs”), to be submitted by COP-16. The majority of targets identified in the pilot, center around water, land use and atmospheric emissions, showing how targets set as part of TCFD and SBTi implementation have been adapted for use in TNFD disclosures.

Table 10: Examples of pilot members’ targets

Sector |

Global Architecture |

Local Assessment |

|

Energy

|

‘We commit to producing a net positive impact on biodiversity, confirmed by a third-party institution, for each new project on sites located in an area of priority interest for biodiversity, that is, IUCN (“International Union for the Conservation of Nature”) Protected Area Categories I to II and Ramsar areas.’

|

‘Reduce the freshwater withdrawal of the sites located in water stressed area by 20% between 2021 and 2030’ |

|

Land Use

|

‘Add 100 thousand hectares for conservation and/or protection by 2030 from a 2018 baseline’ |

‘All tobacco growing areas to perform a local water risk assessment and develop mitigation plans by 2025’ |

|

Built Environment

|

‘Reduce our freshwater withdrawal specifically related to cement by 33% by 2030 from our 2018 baseline’ |

‘Making 25% of manufacturing facilities (individual sites) landfill-free by 2025’ |

For specific guidance on interim targets for different systems, see Roadmaps to Nature Positive, Foundations for Built environment, Land-use: agri-food (row crops) and forest sectors and , Energy systems.

A roundtable discussion between Financial institutions (FIs) and corporates was held to understand how FIs are integrating corporate nature-related disclosures into their decision making, and how implementing TNFD guidance will support corporates to meet FI requirements. FIs outlined their approach to implementing TNFD guidance in practice, highlighting where data from corporate disclosures would feed into decision-making.

The approach to nature-related assessments used by a sample of FIs

During engagement with FIs conducted over the pilot, it was observed that it may not always be possible for FIs to follow the LEAP approach, for example, it was difficult to obtain location-specific data, which is a prioritization criteria for the ‘Locate’ stage of LEAP. This stage was deemed to be too granular for some FIs, and therefore the majority started the LEAP approach with either the ‘Evaluate’ or ‘Assess’ stage following the initial scoping.

The four step risk assessment approach outlined below is a synthesis of methods currently in use by the sample of eight FIs engaged during the pilot, of which, there was a clear variance in maturity. Less mature FIs were solely relying on third-party data as described in step 1 below, whilst more mature FIs were additionally collecting corporate data on material impact drivers, supplementing data gaps with third party tools where necessary (step 2) to allow them to set a materiality threshold (step 3) and take any necessary further action (step 4).

As maturity in this area increases, it is expected that more FIs will be looking to align with TNFD and use corporate information to inform strategic decisions related to nature. TNFD has specific guidance for FIs, including specific metrics. TNFD explicitly states that businesses should disclose the financial implications of material DIROs to enable this decision-making process. Therefore, it is in the best interest of businesses to disclose the necessary information, so that third party tools are not used to supplement data gaps as this may provide the FI with an overestimate of their risk exposure, leading to potential negative consequences for the businesses involved.

Figure 23: A synthesis of the risk assessment approaches used by a sample of financial institutions to date

The FIs also stated that TNFD’s response metrics were useful to measure and compare what actions businesses are taking regarding qualitative factors such as supplier engagement. The response metrics were often cited as a way of deciding what further action needed to be taken.

Moving from LEAP to disclosures

This section focuses on using LEAP assessment outputs to draft TNFD disclosures. Suggestions for improving disclosures were discussed over the course of the pilot program, often informed with input from the TNFD secretariat. Disclosure against the TNFD recommendations is a complex and highly-technical process with mixed maturity amongst members before the pilot (see the ‘Pilot members TNFD Maturity’ section). Significant gaps for certain disclosure recommendations highlight the need for detail and granularity not currently implemented by most businesses.

The TNFD recognizes that nature-related disclosures will be new to many organizations, and that it may be prudent to start with a narrow scope (for example, focusing disclosures on specific operations where nature-related risks and opportunities are most material) and then expand over time. There is an expectation that after no more than 5 years, organizations will be considering all material impacts and dependencies across their direct operations as well as upstream and downstream activities. Therefore, before implementing TNFD guidance, it is important to understand your organization's current level of maturity and ambition. In light of this, the TNFD recommends that an organization provides a statement outlining the scope of disclosures, and what further disclosures are planned in the future.

In order to better understand what an initial TNFD disclosure might look like, actions for each disclosure recommendation were identified for those who are just getting started as well as additional actions that could be taken to assist those who are ready to include more detail. These suggestions provide practical actions for businesses which have been informed by the discussions, workshops and insights gained throughout the pilot program.

Disclosure recommendation |

Actions to help you get started |

Continuing the TNFD journey |

FI expectations for disclosures |

A. Describe the board’s oversight of nature-related dependencies, impacts, risks and opportunities |

Identify specific criteria in the role descriptions of sustainability officers and directors relating to responsibility for management of nature-related issues at the management and board level. |

Upskill the board on the materiality of nature-related issues to ensure that these are integrated into all key decision-making processes. |

Transparency over internal nature-related management and board level structures. |

B. Describe the management’s role in assessing and managing nature-related dependencies, impacts, risks and opportunities |

Upskill management and staff internally on the topic of nature by reading through TNFD resource bank, beginning internal dialogue and engagement across teams, or hiring external experts to provide training on key topics. |

Engage with external partners such as local Non-Governmental Organizations (“NGOs”) to widen understanding on key topics that are material to your organization and ensure these are integrated into wider enterprise risk management processes. |

Transparency over the processes in place to manage nature-related risks and opportunities. |

C. Describe how affected stakeholders are engaged by the organization in its assessment of, and response to, nature-related dependencies, impacts, risks and opportunities. |

Comply with national, regional and local regulations regarding the state of nature. |

Expand ambition beyond compliance with regulations, collaborating with external stakeholders, including Indigenous Peoples and Local Communities (IPLCs) to apply the mitigation hierarchy (‘avoid, minimize, mitigate, offset’) for action. |

Clear classification and scoping of stakeholders, including rights holders, explanation of representation and nature context, including benefit sharing and just transition, for example. |

* Note, disclosure C related to stakeholder engagement was originally considered under Risks and Opportunities in previous beta versions. We have kept insights and feedback related to stakeholder engagement under Risks and Opportunities in this report.

Disclosure recommendation |

Actions to help you get started |

Continuing the TNFD journey |

FI expectations for disclosures |

A. Describe the nature-related dependencies, impacts, risks and opportunities the organization has identified over the short, medium and long term |

Build up a longlist of potential DIROs and qualitatively assess associated time horizons by holding a workshop to engage with relevant stakeholders across the business. |

Expand the assessment to consider how nature-related R&Os might impact other risks e.g. climate-related risks over short, medium and long term.

|

Comprehensive and systematic classification of DIROs at different levels of granularity with appropriate context, reflecting materiality processes and a range of time horizons.

|

B. Describe the effect nature-related risks and opportunities have had and may have on the organization’s businesses, strategy, and financial planning |

Discuss maturity and ambition level with key stakeholders internally to determine level of nature-related risk appetite and which R&Os may impact the business. |

Highlight internally how incorporation of nature-related risks and opportunities can strengthen business strategy, creating a nature-related roadmap to avoid siloed assessment or risks and opportunities. |

Start with current status qualitative descriptions and processes but ideally provide more forward-looking quantitative information on products/services, investment, research and development etc.

|

C. Describe the resilience of the organization’s strategy to nature-related risks and opportunities, taking into consideration different scenarios |

Scenario analysis can be treated as an iterative process, and the scope can be broadened over time. An initial assessment may be qualitative and focus on certain commodities, regions or biomes that are most relevant to the organization. |

The assessment can develop to include material R&Os under different scenarios, as well as considering different magnitudes and time frames. As maturity increases scenarios can become more quantitative providing estimates of financial impacts.

|

Alignment between nature and climate scenarios where possible. Sensitivities (e.g. $ impact or relative % change) provided to key scenario conditions/ parameters.

|

D. Disclose the locations where there are assets and/or activities in the organization’s direct operations, and upstream and/or downstream and/or financed, where relevant, that are in: high integrity ecosystems; and/or areas of rapid decline in ecosystem integrity; and/or areas of high biodiversity importance; and/or areas of water stress; and/or areas where the organization is likely to have significant potential dependencies and/or impacts |

Understand what organizational and value chain location data is already being collected that could be used to inform where priority locations may exist. |

Develop collaborations with nature-related data providers to improve access to location-specific data. |

Clear classification, traceability and appropriate transparency, connecting location with nature of activity and implications/effects. |

Disclosure recommendation |

Actions to help you get started |

Continuing the TNFD journey |

FI expectations for disclosures |

|

A(i). Describe the organization’s processes for identifying and assessing nature-related dependencies, impacts, risks and opportunities in its direct operations A(ii). Describe the organization’s processes for identifying and assessing nature-related dependencies, impacts, risks and opportunities in its upstream and downstream value chain(s) and financed activities and assets for assessment |

Disclose key risks by identifying material dependencies for your sector of operations and translating them into risks i.e. a singular approach to risk identification.

|

Carry out additional risk assessments to identify further risks i.e. use multiple approaches to identify risks. For example, using primary data sources to identify risk hotspots in your operations or value chain.

|

Disclosure of the process for identifying all material nature-related issues for direct operations with the view to expand to look at upstream and downstream nature-related issues. Disclosure of quantitative absolute or relative assessments (e.g. value at risk).

|

B. Describe the organization’s processes for managing nature-related dependencies, impacts, risks and opportunities and actions taken in light of these processes |

Identify a long list of potential mitigation and management actions that can be taken. From this list, identify “no regret” actions that can be taken in the immediate future to help drive momentum. For example, engaging with suppliers in high risk priority locations.

|

Assess varied risk mitigation and management actions through use of the risk mitigation hierarchy. This can be done through ranking actions based on their level of protection and reliability. |

Description of the types of monitoring, reporting and verification (MRV) systems in place, including use of any third-party tools and how decisions are made using these systems. |

C. Describe how processes for identifying, assessing and managing nature-related risks are integrated into the organization’s overall risk management |

Start with nature-related DIROs assessed separately from traditional Enterprise Risk Management (ERM) processes. |

Integrate nature-related DIROs with ERM processes over time. Considering additional assessment criteria and time horizons.

|

Methodologies and material outputs of environmental risk assessments at key sites or for key business lines are clearly integrated into wider ERM processes. |

Disclosure recommendation |

Actions to help you get started |

Continuing the TNFD journey |

FI expectations for disclosures |

A. Disclose the metrics used by the organization to assess and manage material nature-related risks and opportunities in line with its strategy and risk management process |

Start with qualitatively assessing DIROs, using third party tools and engaging with stakeholders to understand materiality through a ‘top-down’ approach i.e. without inclusion of any corporate data. For example, this might involve use of sector or country averages. |

Organizations that are more mature can aim to quantify their identified DIROs using a ‘bottom-up’ approach which incorporates company-specific primary data. For example, nature-related impact drivers such as water consumption will show a more accurate reflection of impact. |

Overall mix of risk exposure, sensitivity and opportunity investment, resourcing, development sought. Important to disclose metrics to assess and manage risks and opportunities in high-risk areas e.g. Key Biodiversity Areas (KBAs). |

B. Disclose the metrics used by the organization to assess and manage dependencies and impacts on nature |

Narrow the scope of data based on what is material to your organization. For example, focusing on water use in water scarce regions if water is a material dependency. In addition, proxy indicators can be used to signal impact levels such as measuring soil organic carbon as a proxy for soil health. |

The scope can be expanded over time to include metrics that manage these impacts and dependencies at priority locations. For example, the proportion of sites producing nature action plans (%).

|

Examples of metrics some FIs look for: ● Hectares of land use change to prioritize conservation or restoration; ● Certified percentage of sustainably sourced soft commodities. |

C. Describe the targets and goals used by the organization to manage nature-related dependencies, impacts, risks and opportunities and its performance against these |

Set targets related to material impact drivers. Some organizations decide to approach target setting by focusing on specific impact drivers and/or areas of key pressure that are relevant to their value chain. |

Expand target-setting to include actions that drive nature-positive outcomes. For example, targets for nature-related opportunities regarding land restoration, rather than focusing on minimizing nature-negative outcomes. |

Examples of targets some FIs look for: ● ‘Zero deforestation’ target ● Context based water use target ● Targets relating to land use restoration and recovery

|