Real estate is the world's most valuable asset class representing two-thirds of global wealth. With more than 13% of global GDP related to construction and 12% of employment, its size means it is responsible for an astonishing 40% of global energy-related carbon emissions (14 Gt per year). This is because it makes up over one-third of global final energy use and consumes 40% of raw materials globally. Achieving net-zero carbon emissions in the built environment by 2050 will require investments of USD $1.7 trillion annually and will create half a million more direct jobs.

Real estate assets are a valuable and growing component of institutional investment portfolios. At the same time, ambitious policies and regulations, changing public awareness and radically shifting demand drivers are pushing finance sector stakeholders to focus on sustainability in their portfolios because it affects business in the short, medium and long term. When put together, the finance sector has a unique opportunity to shape demand and drive transformation in the built environment.

Achieving net-zero emissions in the built environment by 2050 is the last stop along an arduous path. The specific targets all actors need to aim for are for all newly constructed buildings to have net-zero operational emissions by 2030 and for all buildings – including existing ones – to have net-zero emissions by 2050. And embodied carbon emissions – emissions from material production and construction processes – must be at least 40-50% lower by 2030 than today and net zero by 2050. Unfortunately, we are not on track.

Halving emissions by 2030 is, therefore, the first stop and must effectively happen today. This is because the lead times in typically built environment projects can easily be 8 to 10 years, so companies planning and designing projects today must already include these targets for 2030.

Achieving this massive transformation at the speed and scale required means that all actors have to share the same vision of halving emissions by 2030 and reaching net zero across the entire life cycle by 2050. They also must deeply and radically collaborate to realize this vision – across governments, the finance sector, businesses along the full value chain, science and civil society. The collaboration needs to focus on the following three critical levers for market transformation (WBCSD and GlobalABC, 2021):

- Adopt whole-life carbon (WLC) and life-cycle thinking and concepts across the value chain and the market to align on key indicators, metrics and targets consistently.

- Treat carbon like cost: Internalize the WLC emissions costs and reflect them in the price of products and services throughout the value chain, including in governance mechanisms, procurement and taxonomy, from governments and the financial sector.

- Foster a positive and reinforcing supply and demand dynamic that incentivizes low-carbon solutions along the value chain. This requires signals from government and finance and, most importantly, collaboration between industry players along the whole value chain.

The role of the finance sector

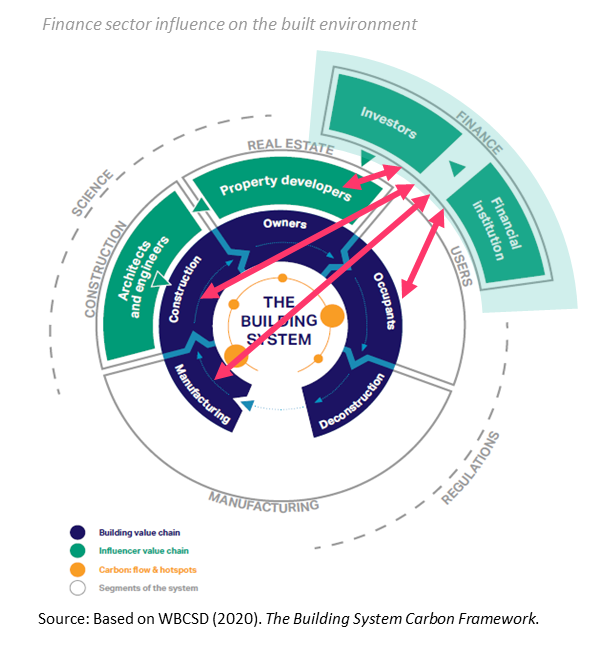

Finance sector stakeholders strongly influence built environment impacts through loans and investments in built assets and – indirectly – investing in value chain businesses. When mobilizing financial capital, they can set requirements for low-carbon solutions in building projects and across the value chain. Investors, asset managers, banks, advisors and insurers all influence if and how buildings are constructed. They play a crucial role in the very early stages of buildings when decisions significantly impact their future emissions. This includes the energy performance of buildings and setting requirements to reduce emissions from building materials and the construction process.

To understand how the finance sector can exert this influence, let's look at what holds us back today.

Challenges and opportunities

The transition's challenges are many and complex. For instance, there is a lack of true collaboration and understanding between the construction, real estate and finance sectors, despite their deep link and reliance. Poor data availability, quality, and limited transparency are holding up measurement, benchmarking, and target-setting processes for net-zero emissions pathways. The built environment and finance sectors are facing a skills shortage in terms of understanding, writing and using reporting and disclosure documents effectively to determine how the results could drive investments. And financial services organizations have traditionally prioritized short-term financial returns over positive, but more difficult to assess, environmental, social and governance (ESG) returns.

However, in all of these, there are opportunities. Stakeholders can find new ways of working together, and legally binding contracts, for example, can help ensure the right incentives, procurement methods and metrics to support net-zero emissions goals for project delivery (see WBCSD's Decarbonizing construction – Guidance for investors and developers to reduce embodied carbon).

Alignment on the growing number of guides, standards, tools and certifications for assessment and reporting would ensure data availability, quality and transparency (note World Green Building Council's (WorldGBC) BuildingLife project, the RICS professional statement on whole life carbon, and the Ashrae-International Code Council (ICC) Whole Life Carbon Approach Standard).

Training and upskilling on sustainability-related disclosures and strategies to align with the Paris Agreement would ensure investors and built environment professionals see the value in these documents from both sides. They would become part of the central decision-making process for investments, linking non-financial concerns with financial impact. The Urban Land Institute (ULI) Europe's C Change project, which is currently addressing transition risk in valuation, is an example of progress in this area. Changing the corporate culture will further the idea that the ultimate goal is to ensure strong returns on investment while creating value beyond shareholders, managing the multifaceted risks of transitioning to net-zero emissions and safeguarding people and the environment.

Understanding these and other challenges and opportunities will help the sector adapt strategies and solutions that will be the key to achieving net-zero emissions.

No-regret actions for finance sector stakeholders

Four specific interventions sit at the core of strategies to reduce the full life-cycle emissions of projects in the built environment: Accountability, Ambition, Action and Advocacy.

- Finance stakeholders in the built environment can achieve accountability through standardized data measurement and transparent reporting.

- In setting credible, science-based net-zero emissions targets, they raise ambition.

- They take action by developing climate transition plans and placing whole-life carbon at the center of decarbonization strategies and decisions.

- By working with the public sector and organizations like WBCSD and its partners in the BuildingToCOP Coalition and Global Alliance for Buildings and Construction (GlobalABC), they place advocacy for policies and regulations targeting sustainable finance at the heart of efforts to level the playing field for the market.

For asset owners and investors, achieving the transition means setting clear portfolio- and asset-specific targets and timelines. They also must embed critical climate and ESG factors into requests for proposals, investment mandates, manager selection and stewardship engagement with portfolio companies and incorporate the related risks (and opportunities) into valuations and, ultimately, into investment decisions.

For asset managers, the lack of consistent, comparable and decision-useful information on climate impact is still a barrier to better implementation. However, growing demand and regulatory pressures motivate every firm to overcome data challenges through proprietary work or third parties. Standardized frameworks and local/regional taxonomies help the asset management industry with enhanced tools for assessment, benchmarking and reporting. WBCSD's Net-zero buildings – Where do we stand? report lays the basis for a harmonized whole-life carbon assessment and reporting framework.

Finance providers can acquire a better understanding of the emissions from the products they are financing using adequate data, tools and standards, including the cost of carbon and transition risk considerations. The ability to accurately measure and standardize (whole life) carbon emissions could help them link their financial offerings to carbon targets and potentially provide lower costs for low-carbon projects. For that to happen, they need clear and transparent information to reliably assess the business case and build trust with the market.

For insurance providers, it means developing methodologies to assess and quantify different climate change scenarios and integrating both physical and transition risks into decisions to enter or exit an underwriting.

Lastly, investment advisors and data providers can facilitate top-down learning as they share and spread best practices and become significant players in the standardization and harmonization of data and target-setting (including but not limited to the Carbon Risk Real Estate Monitor (CRREM), Science Based Targets initiative (SBTi) and GRESB).

What's next? Achieving a breakthrough in buildings

To reduce built environment emissions globally from 14 Gt per year to 7 Gt per year seems to be a daunting task. However, with a clear focus on whole-life carbon emissions alongside cost, the finance sector can help accelerate this transition. There is evidence that we can reduce construction emissions by half today and cost-effectively. And evidence is also emerging that retrofitting building portfolios to net-zero emissions can be achieved competitively.

What needs to happen next is for all stakeholders – finance, national and local governments, and businesses along the value chain – to come together and co-develop roadmaps for a net-zero built environment that identify a clear vision, actions and accountability. Building on the aforementioned built environment market transformation levers, they can drive a united response and decisive action, thereby overcoming the fragmentation of efforts seen so far. The emerging Buildings Breakthrough with national governments committed to transforming their built environment will provide a platform to join efforts and collaborate to achieve a future in which the built environment turns from a problem into a solution to tackle climate change.

We cannot wait – because for the built environment, 2030 is today.